Impacts, vulnerability, and adaptation to climate change by the insurance industry

Climate change poses an enormous challenge to society on two interconnected fronts: strategies to reduce greenhouse gas emissions are needed to bring its causes under control, while at the same time, to address its consequences, adaptation strategies to protect against the effects of a hotter, more extreme, and more unpredictable climate, effects that are already in evidence, need to be implemented.

Insurance is a strategic sphere of activity in the battle against climate change. First, it is a fundamental means of transferring risk, enabling society to enhance its ability to recover after the damage caused, for instance, by climate-related events. Second, insurance may play a key role by developing strategies to mitigate and adapt to climate change, helping to transition to a low-carbon society resilient to its unavoidable impacts. Nevertheless, climate change is also a grave menace to strategic economic sectors such as the insurance industry, because it is associated with an increase in certain physical hazards that can pose challenges to its business strategies and compromise the sector's long-term sustainability.

The first

National Climate Change Adaptation Plan (in Spanish PNACC, Plan Nacional de Adaptación al Cambio Climático), approved in 2006, included insurance among the vulnerable industries and considered the need to assess the sector's impacts, vulnerability, and adaptation. Since then a series of actions have been taken regarding adaptation and the insurance sector. One such action was a meeting held in 2017 in the framework of a programme of ongoing PNACC seminars to give scientists and insurance professionals an opportunity to exchange knowledge on the impacts of climate change and adaptation to climate change by the insurance industry in Spain. Some of the main conclusions reached were published in an

article in issue number 8 of this journal in the spring of 2018. That seminar gave a major boost to knowledge generation on the topic and resulted in an initial proposal of content for granular analysis of the impacts, vulnerability, and potential adaptation measures in the field of insurance activity in Spain.

Pursuing this process further, in 2020 Spanish Climate Change Office issued a report entitled

"Impacts, vulnerability, and adjustment to climate change by the insurance sector" [Impactos, vulnerabilidad y adaptación al cambio climático en la actividad aseguradora]. The report was based on a wide-ranging review of the literature on the insurance industry and its relationship to climate change at both the national and international levels. Like the seminar in 2017, certain key players in the sector in Spain took part and conveyed their thoughts on the matter through interviews. The report addresses some of the challenges from climate change faced by the sector and considers possible adaptation measures for the insurance industry and opportunities for it to help build resilience. Furthermore, it identifies certain emerging issues of interest to the sector and certain gaps in knowledge that should foster reflection, discussion, and engagement on the part of players involved in the insurance field. In many cases, this is already finding a foothold in international forums and national initiatives.

The report discusses the national and international context of climate change, identifies relevant global climate hazards facing the insurance sector, and gives examples of management in such countries as the United Kingdom, the United States, Canada, and Australia. After examining the characteristics of the sector in Spain and its special features compared with other countries in our milieu, it sets out national forecasts on climate change, assesses the possible impacts on and vulnerabilities of the insurance sector (in response to such events as flooding, drought, and heatwaves), and identifies the key players involved. Lastly, it compiles some current and potential contributions of the insurance business to adaptation generally, assesses the viability of the sector and possible measures to help it adapt, and identifies knowledge gaps.

One of its chief

conclusions is that globally the insurance sector is experiencing an increase in the frequency and intensity of events associated with relevant climate hazards. The damage they cause is also on the rise, though for the time being this trend is associated basically with increased exposure resulting from extensive urban transformation and economic development worldwide. In recent years events associated with secondary hazards (fires, flooding caused by cyclonic storm surges, etc.) have become more commonplace and more intense, and these secondary hazards have sometimes caused greater damage than the primary hazards, highlighting the need to improve the predictive models for these hazards. Nevertheless, the insurance sector considers that at the present time it has the capacity and sufficient solvency to cope with the climate-related perils associated with global warming in the short term thanks to ongoing upgrading of its activities.

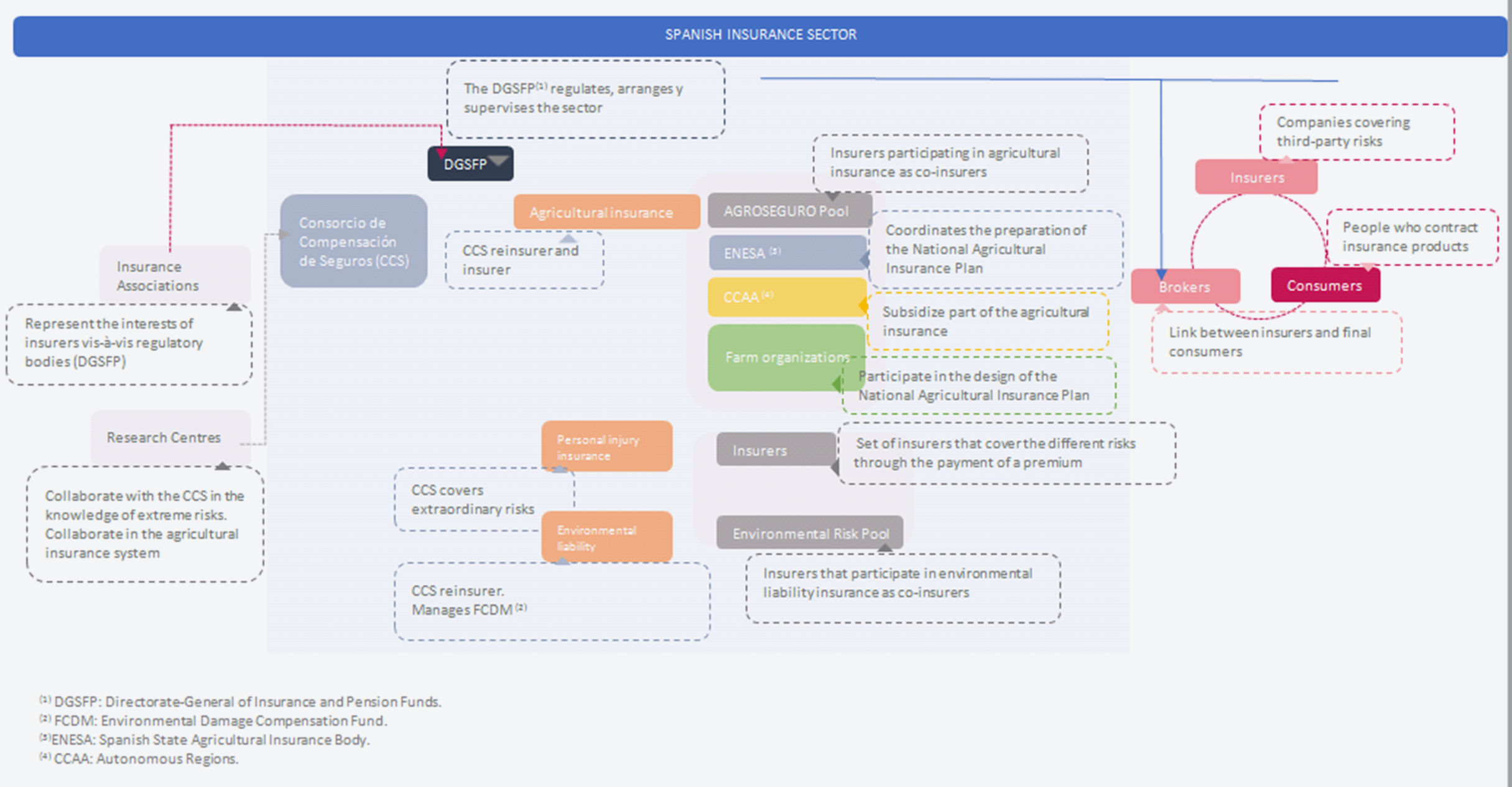

Transposing that analysis onto the situation in Spain, it should be borne in mind that all climate perils, from the risks associated with such events as flooding and storm surges to those involving hail, drought, forest fires, and heatwaves, are affected by climate change to a greater or a lesser extent, which may in turn affect loss rates in most lines of insurance. The impacts of climate change in Spain may therefore affect both the coverage of the so-called 'extraordinary risks' by the Consorcio de Compensación de Seguros (CCS), agricultural insurance, and many other lines, e.g., life, health, accident, vehicle, and travel medical insurance.

Figure 2. Diagram summarising the structure of the insurance industry in Spain.

Source: "Impacts, vulnerability, and adjustment to climate change by the insurance sector" report.

Nationally, the main climate perils affecting the sector are flooding and wind storms, natural phenomena that come under the extraordinary risk covers provided by the CCS. In the CCS's view, for the present the current system of coverage does not require changes based on the results of studies that have been carried out and the reserves on hand, despite the growing frequency and intensity of exceptional climate events.

Multi-peril agricultural insurance is likely to be most affected by climate change because of the farming sector's heavy dependence on climate factors, but by the same token it is one of the lines with the greatest capacity for adaptation. The main climate perils affecting agriculture are drought and hail, which for several consecutive years have caused catastrophes requiring recourse to the CCS's reinsurance capacity. In this connection, the system's flexibility and ongoing research studies, while at the same time promoting the necessary adaptation measures, will be vital to the long-term sustainability of multi-peril agricultural insurance.

The conclusion reached concerning other climate hazards not covered by the CCS's extraordinary risk scheme or multi-peril agricultural insurance was that there was insufficient disaggregated data on the climatic or environmental circumstances associated with these losses, making it hard to forecast the possible impacts of climate change. This could delay the development of any suitable adaptation strategies that may be required.

Turning to options in response, there was found to be a need to boost scientific research and to transfer scientific knowledge to the insurance sector. The main purpose would be to ascertain in detail the effect of environmental changes on existing perils and to identify emerging new perils in both the short term and the long term. This knowledge is essential to be able to undertake the required adaptations to the system, to design new products to cover the new risks without endangering the system's sustainability, and to generate new opportunities for the insurance sector to make it more innovative and resilient.

The Spanish insurance system, with its broad experience and special structure marked by public-private cooperation, is taken as an example of success internationally. It enjoys enormous potential to exert influence and take the lead in introducing sustainability measures into its business model in the current context of climate change and so bring social, economic, and financial stability to society.

The struggle against the effects of climate change is one that requires joint, coordinated efforts by all the players that can help the different sectors adapt to climate change. Commitment by public bodies, insurance companies, associations, research centres, and the private financial sector is essential to meet the challenge of adaptation in the insurance sector. A key mechanism for understanding climate change and taking action would be to set up new frameworks for cooperation and jointly promote initiatives to adapt to the risks, from exchanging information on trends in the various risk components (peril, exposure, vulnerability), to resilient recovery (employing "build back better" strategies), to potentially creating special financial instruments to reduce catastrophe risks.

Moving from knowledge to action: the National Climate Change Adaptation Plan (PNACC) 2021-2030 and the new EU Strategy on Adaptation to Climate Change

While knowledge generation on adaptation to climate change is still regarded as a priority, especially in areas with major knowledge gaps like those mentioned above, there is a growing consensus as to the urgent need to identify and implement effective measures to limit the risks arising from climate change and to increase the level of resilience on the basis of the knowledge that is already available.

The recently approved

National Climate Change Adaptation Plan (PNACC) 2021-2030 recognises this priority and includes guidelines for action on cross-cutting issues to be addressed in order to be able to advance with adaptation. This new PNACC for 2021-2030 was approved by the Council of Ministers last September and is a basic planning instrument for promoting coherent, coordinated action to tackle the threats and hazards posed by climate change in the different spheres of society based on a multi-level (on different territorial scales), cross-cutting (across different sectors) approach. That is, the PNACC 2021-2030 is aimed at averting or reducing present and future damage brought about by climate change and at building a more resilient economy and society.

Figure 3. Cover of the PNACC 2021-2030.

This second PNACC is part of a strategic energy and climate framework, a package of instruments that encompasses the Energy Transition and Climate Change Act [Ley de Cambio Climático y Transición Energética]; the long-term strategy towards achieving a modern, competitive, climate-neutral economy by 2050; the Integrated National Climate and Energy Plan 2021-2030 [Plan Nacional Integrado de Energía y Clima 2021-2030]; and the Just Transition Mechanism [Estrategia de Transición Justa]. This material also addresses adapting to climate change and is clearly connected to the PNACC.

The PNACC 2021-2030 contains major new developments and new ways of viewing adaptation governance in our country. To wit:

- It emphasises the need to consider a series of guiding principles that should inform adaptation policies and measures, such as taking into account the territorial and social dimensions and taking the best available knowledge and science as a basis.

- It sets out 81 courses of action for different sectors arranged into 18 working areas, chief among which are human health; water and water resources; farming and livestock raising; and cities, urban development, and building; not to mention insurance activities and the financial system.

- It specifies 7 cross-cutting issues to be promoted in the various working areas.

With respect to the financial system and insurance industry, the new PNACC puts forward four specific objectives:

- Promoting the role of the financial system as a catalyst for adaptation to climate change and further exploring and fomenting specific contributions to adaptation by the insurance industry, placing special emphasis on agricultural insurance and on establishing incentives for risk prevention.

- Fostering the generation of knowledge and skills with regard to the impacts of climate change on the financial system and the insurance sector and identifying investment opportunities for contributing to adaptation to climate change.

- Promoting measures for adapting to the financial risks associated with climate change by means of assessment, dissemination, and prevention.

- Supporting frameworks for cooperation and partnering with regard to adapting to climate change by the different actors involved in the financial system, placing special attention on the insurance sector, and buttressing the sector's adaptation capabilities.

Four courses of action have been put forward to achieve these objectives, intended to promote making adaptation to climate change a part of sustainable finance initiatives, creating incentives for risk prevention by integrating adaptation into insurance activities, implementing stable frameworks for coordination and cooperation with key actors in the financial system and the insurance field with respect to adaptation, and strengthening these sectors' adaptation capabilities.

The European Commission, in its turn, has recently presented the new EU strategy on adaptation to climate change — Forging a climate-resilient Europe. The new strategy sets out how the European Union can adapt to the unavoidable impacts of climate change and become climate resilient by 2050, setting four main objectives: making adaptation smarter, swifter, and more systemic and stepping up international action for adaptation to climate change. Like the earlier 2013 Strategy on Adaptation, the Commission has underscored the connection between adaptation and insurance, expanding its previous proposal, which consisted of promoting insurance and other financial products with a view to investment decision-making and resilient enterprises.

In the context of smarter adaptation, with a focus on improving knowledge and managing uncertainty, the new European Strategy sets out the need to acquire more and better climate-related risk and losses data. The Strategy proposes that the European Commission, together with the European Insurance and Occupational Pensions Authority (EIOPA) and the industry, should study the best ways to collect comprehensive and harmonised data on insured losses.

As concerns swifter adaptation, it aims to step up adaptation in all areas and includes a section specially dedicated to Closing the climate protection gap. In this connection it states that in the context of the Renewed Sustainable Finance Strategy, the European Commission will:

- help to examine natural disaster insurance penetration in Member States, and promote it, for example, through guidelines, and invite EIOPA to develop its natural catastrophe dashboard allowing country level assessments;

- strengthen dialogue between insurers, policymakers, and other stakeholders;

- identify and promote best practices in financial instruments for risk management, in close cooperation with EIOPA;

- explore the wider use of financial instruments and innovative solutions to deal with climate-induced risks.

Both the PNACC 2021-2030 and the new EU strategy on adaptation to climate change are intended to drive adaptation policies ahead and to strengthen the role of the insurance sector in this process. They also represent a major step forward towards developing specific measures for an urgent and suitable response to the climate emergency we are currently facing.