Agricultural insurance has a long track record in Spain, permanently seeking solutions that provide a balance between protection for farmers and insurance technique. The sector is clearly complex, with a very varied range of productions exposed and susceptible to the effects of a large number of hazards. The Combined Agricultural Insurance System has proven to be, since the end of the seventies, and through an on-going process of adaptation and improvement, a balanced and stable solution, in which together with the insurers (grouped in AGROSEGURO), the insured themselves participate, through professional agricultural organisations and cooperatives, as well as various public bodies (ENESA, departments of the Autonomous Communities, the Directorate-General for Insurance and Pension Funds, and the Consorcio de Compensación de Seguros).

Ignacio Machetti Bermejo

President of Agroseguro

1. The background

Spain’s specific meteorological characteristics and the adverse effects of the different natural phenomena on crops and livestock breeding lie at the source of the birth of the agricultural insurance system in this country, and its subsequent development. At the beginning of the twentieth century, a score of companies operated in Spain, insuring harvests against the risk of fire. Some Friendly and Mutual Societies which insured livestock were set up, while some foreign-capital enterprises offered protection against hail. In 1917, the Mutual Insurance Bank against Hail was set up, and the Ministry of Development, which handled farming affairs, appointed a Commission which put down the bases for a National Insurance Mutual Society specialised in hail.

Since then, and until passage of the Combined Agricultural Insurance Act in December 1978, many attempts were made to apply insurance technique to cover all risks affecting agriculture and livestock production.

In 1919, the National Mutual Society for Agriculture and Livestock Insurance came into being. It underwent subsequent transformations and changes of name -Commissioner’s Office for Country Insurance, the Agricultural Insurance Service- until it was converted in 1934 into the National Country Insurance Service. The impossibility of balancing indemnifications for insured losses and collected premiums meant that this Service posted a permanent deficit until 1953. That year the Country Insurance Act was passed, entrusting agricultural insurance to private enterprise, one year before passage of the Act which created the Consorcio de Compensación de Seguros. Since then, the need has grown for an integral agricultural insurance able to protect from multiple risks.

It was not until the seventies that there was a significant change in national agricultural insurance. The political and economic situation of those years, along with the 1973 and 1974 farming campaigns, led to the creation of a Pool (known as the National Cereals Insurance Coinsurers Pool) which united insurers to administer combined insurance.

Finally, Act No. 87/1978 of 28 December, the Combined Agricultural Insurance Act, was passed -democratic Spain’s first Act of Parliament-, and it was developed a year on in Royal Decree No. 2329/1979 of 14 September, passing its Regulations.

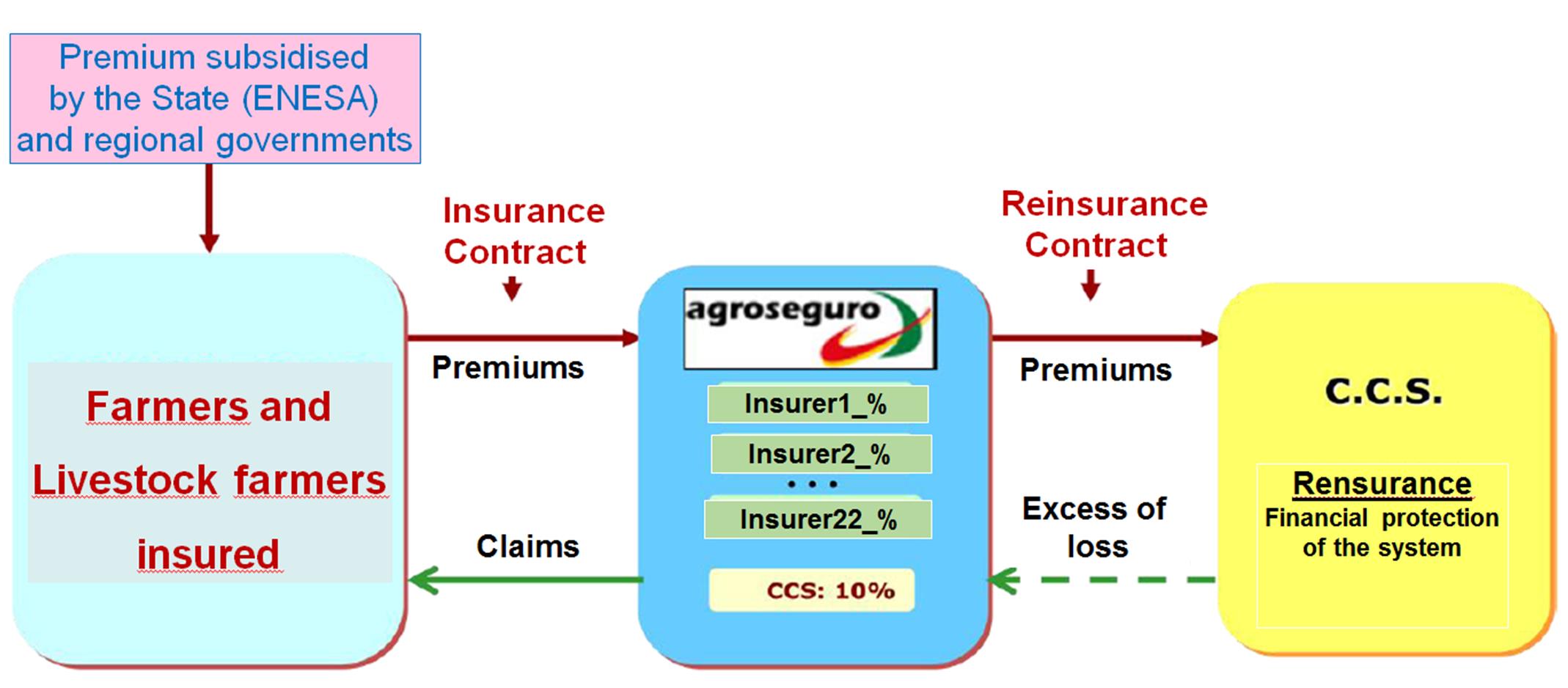

The new Act led to the creation of a series of institutions which, in addition to other players, have contributed a unique value and significant stability to the Spanish agricultural insurance system. This is a system jointly involving private insurance companies and public institutions, and it is based on the voluntary participation, both of the insurance companies and of the farmers and livestock breeders themselves. The premiums are heavily subsidised, fundamentally by the Central Administration and later, in addition, by Regional Governments.

2. A general description of the spanish combined agricultural insurance system

The agricultural insurance system in Spain constitutes a tool enabling farmers and livestock breeders to confront the risks which directly and very severely affect their operations -such as meteorological risks, accidents, diseases or epizootics-, allowing them to continue with their businesses.

This system of insurance is the upshot of collaboration between public institutions and private entities whose respective roles have developed, strengthened and consolidated with the passage of time as the system has grown in volume, range of cover and efficiency. Thus the participation of the system’s various players can be summarised as follows:

a.- The Central Administration

In the public sector, the body coordinating the operation of the system is the

State Agricultural insurance Corporation (ENESA) in the Ministry of Agriculture, Food and the Environment (MAGRAMA) whose functions include the drafting of the Annual Agricultural Insurance Plan and its subsequent referral to the Government, the management of the subsidies for insurance premiums, and the coordination with Regional Governments in this matter.

One of the characteristics of the Spanish Agricultural Insurance system is the participation of the Public Administrations in the cost of the insurance, i.e. the State contribution by means of a direct subsidy to farmers or livestock breeders to meet part of the premium. This state contribution has been and is decisive in guaranteeing the system’s implementation.

Initially, the subsidies were funded almost exclusively from the General State Budget, until complemented by those granted by Regional Governments in line with the budget resources available at any time.

It is important to highlight on this point an instrument which illustrates the degree of collaboration between the public and private sectors in this system, in the form of Agreements for the settlement of subsidies concluded with ENESA and the Regional Governments so that, at the moment when the insurance is contracted, the farmer or livestock breeder is able to pay just the net cost, that is the final cost of the insurance less the state and regional subsidies applicable in each case.

For ENESA, the percentage of the subsidy to be assigned to each insured party is calculated from a base subsidy that varies depending on the production insured and the insurance option contracted. This base subsidy subsequently rises according to its beneficiary’s characteristics (farming as main activity, a young farmer, previous years’ contracting, etc.).

That subsidy, covering part of the cost of the insurance not met by the insured party, is later settled with AGROSEGURO in the procedure provided for in the Agreement.

For the Ministry of the Economy and Competitiveness, the

Directorate-General of Insurance and Pension Funds (DGSFP) is the body which supervises the insurance companies and also approves the composition of the coinsurance table, ensuring as part of this job that the insurers making it up are solvent. It also participates in the drafting of appraisal standards, and proposes to the Ministry the rules governing the reinsurance mechanism implemented by

Consorcio de Compensación de Seguros. This last one is a public business institution which, in addition to acting as compulsory reinsurer, controls the appraisals of losses declared.

The Consortium’s role as reinsurer is particularly notable. Because of the high volatility (variability) of agricultural risks and so of the results of the insurance, it is an essential requisite that the protection offered by the reinsurance should be on-going and stable over time, something which cannot be guaranteed on the international reinsurance market which does not take long-term predetermined relations, making decisive a public reinsurer’s role.

In addition, the Consortium is a member, as one more coinsurer, of the insurance companies’ grouping, enabling it to participate directly in the management of agricultural insurance, although it does not engage in the marketing of policies.

b.- Regional Administrations

The Autonomous Communities collaborate through their Agricultural Councils with the Ministry in drawing up the Annual Agricultural Insurance Plan, coordinating the Territorial Insurance Commissions and, as already explained, granting additional subsidies.

c.- The Production Sector

On the private sector side, the farming sector is represented by the Professional Farming Bodies and the Cooperatives, which bring to the institutions’ notice the particular needs for protection in each area of production, collaborating in the design and planning of the various lines of insurance and performing significant work in publication, frequently acting as agricultural insurance policyholders. In fact, the figure of the policyholder has, in a field of insurance where contracting is in virtually all cases collective, taken on a predominant role in agricultural insurance. Initially handled by Cooperatives, Rural Banks and Agrarian Chambers, those first two have continued to affirm and consolidate the part they play while the profile of the Agrarian Chambers as insurance policyholders has gradually declined as a result of the loss of their functions to represent, claim and defend the professional and socioeconomic interests of farmers and livestock breeders, a role which has been taken up by the freely constituted Professional Organisations.

These Professional Farming Organisations have focused their activity in two directions:

- As policyholders, regarding the collective policies, for and on behalf of farmers and livestock breeders.

- As full members of the Commissions and Working Groups where the various categories and covers of agricultural insurance are debated and designed.

d.- Insurance Companies

For their part, private insurers, grouped in a Pool called the

Agrupación de Entidades Aseguradoras de los Seguros Agrarios Combinados, S.A. (AGROSEGURO), subscribe the insurance and assume the risk, with the same percentage participation in that grouping as the risks they cover, itself directly linked to the policies they contribute to the coinsurance table. There are at present 22 participating in the Pool.

AGROSEGURO, as management company acting on behalf of the insurers, has the task of drawing up the terms and rates for insurance contracts, managing and the contracting of policies by the companies, along with the subsidies from the Public Administrations under the associated Agreements which allow the recipients – farmers and livestock breeders – to meet the net sum of premium subsidies on contracting the insurance. Finally, it also undertakes the management, processing, valuation and payment of losses declared.

The following is the system's general operating pattern:

Overall and from the outset, the system as a whole rests on the following basic principles:

- The universality as for insurable types of production and risks.

- The universality also as for producers’ access to insurance, provided that they meet the conditions for that, which basically are the professional nature of their activity and the application of minimum cropping technical conditions.

- Voluntary participation of farmers and livestock breeders in the insurance.

- Damage caused by insurable risks may not be the subject of extraordinary aid.

- The solidarity of all those involved in the system, and of society itself.

- Application of insurance techniques.

- The financial solvency of the system thanks to the creation of a Pool of insurers which takes on the risk in a coinsurance regime and managed by Agroseguro, and thanks to the reinsurance by the Insurance Compensation Consortium (CCS).

- On-going review and perfection of the system.

Participation in this system offers significant advantages for both public and private sector players:

a) For the farming sector:

- It eliminates uncertainty for farmers and livestock breeders, providing them with cover which guarantees the continuity of their operations by compensating their damage in case of loss so they do not need to depend on any aid and subsidies the State might grant and which, aside from their uncertainty, are directly linked to the occurrence of more or less generalised catastrophic events.

- It assures them that compensation will be adjusted to the loss suffered and the cover contracted, and that it will arrive in a maximum of 60 days following harvest or the end of guarantees.

- It ensures maintenance of a level of income which, in addition to guaranteeing the continuation of operations, stimulates the production of the most suitable crops according to the criteria of the Administration’s economic policy, and of the market.

- It reinforces producers’ solvency in dealing with financial institutions and private individuals.

- It encourages farmers to associate, and introduces business criteria into their operations.

- Finally, it guarantees universal access to insurance.

b) For the Public Administrations:

- It makes it possible to allocate in advance budget items, as appropriate, in order to cover a portion of the premiums to be paid by the agricultural sector, and in order to cover the excess of loss. This offers an alternative, far more effective and efficient, to disaster aid.

- Being based on strictly technical and objective criteria for loss appraisal and valuation, it makes it possible to adjust the indemnification received to the loss suffered, avoiding unjust situations which might otherwise occur, while reducing the economic and political cost, because the criteria for the distribution of payment of indemnification are taken on by all parties.

- Finally, it enhances the financial solvency of the insured themselves, facilitating the State’s own credit policy, using insurance as a guarantee.

In short, given the risks that affect the agriculture and livestock sector, insurance is the best alternative to a policy of disaster aid, and farmers and livestock breeders are therefore tremendously aware of its need, increasingly taking it on as a fixed operational charge, illustrated by the high levels at which it stands in the main productive sectors.

Since the system was initiated in 1978, the Public Administrations, farming organisations and insurance companies have worked permanently to adapt the system to trends in agriculture and livestock practice, year by year incorporating measures which improve the conditions of insurance and give positive responses to the sector’s needs.

3. Trends in contracting in the agricultural insurance system

The system has evolved, incorporating productions and risks gradually. Since its inception, all participants have worked to bring agricultural insurance ever closer to the farming sector’s real cover needs. Thus, with the passage of time, the various insurance lines have been constantly modified, new ones have been created, and the management systems have been revised so that it can be said that, at this time, practically all plant production has, as a minimum, basic covers for selection. A large part of the country’s livestock species are also in this situation.

By way of historical reference, the first Combined Agricultural Insurance Plan was approved by the Council of Ministers on 30 May 1980, and included the following lines:

- Comprehensive Dryland Winter Cereal Insurance (an experimental plan for 10 districts with 50% cover), for frost, drought, flood and hot and/or hurricane-force winds from the moment when stems began to lengthen in the 1981 harvest.

- Insurance for the wine grape for the whole of Spain, with 100% cover for hail.

- Insurance for the apple throughout Spain, with 100% cover for risk of hail.

- Country-wide tobacco insurance, with 100% cover against hail.

- Combined insurance for citrus (orange, mandarin, lemon and grapefruit) for 15 provinces, giving cover against frost (50% cover) and hail (100% cover).

The progressive enlargement of the system toward new plant and animal productions has been uninterrupted since then, so that it can now be said that there is no productive agricultural or livestock sector without cover of the main risks affecting them. In fact, following the grouping in productive sectors of the more than 140 lines of insurance which made up the system in 2011, deriving from introduction of the new management system called “recent insurance”, agricultural insurance has 27 agricultural lines, 15 for livestock (plus cover for removal of carcasses), 4 for fish farms and one for forestry, covering virtually all production and the risks affecting agriculture and livestock operations. Thus:

a) For harvest risks, agricultural insurance contemplates the following:

- Frost.

- Fire.

- Flood.

- Rain.

- Hail.

- Drought.

- Hurricane-force or hot winds.

- Other climatic adversities (the remainder).

b) For risks to livestock:

- Accident.

- Disease or epizootics.

- Pasture drought.

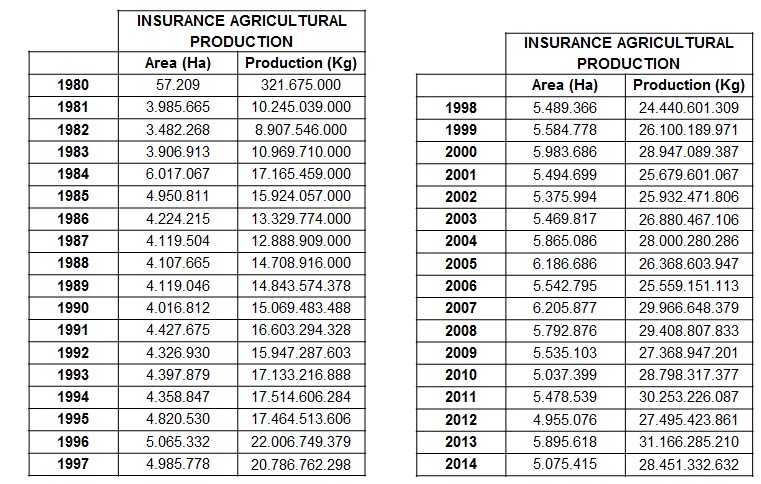

As new productions and risks have been included, the volume of area and production insured has increased exponentially. The tendencies in both magnitudes are shown on the following table:

On the other hand, also in terms of volume of premiums, trends in agricultural insurance have been most significant, as the following table shows:

EARNED PREMIUMS AND RECEIPTS |

SERIES

|

COMMERCIAL PREMIUMS |

TOTAL RECEIPTS

|

ENESA & REGIONAL GOVERNMENT SUBSIDIES |

CHARGED TO FARMERS |

| 1980-92 |

817,516,467.76 |

1,030,793,995.99 |

542,695,195.99 |

488,098,800.00 |

| 1993 |

141,720,678.74 |

184,117,909.10 |

112,721,459.32 |

71,396,449.78 |

| 1994 |

164,504,017.38 |

213,912,334.73 |

127,196,760.53 |

86,715,574.20 |

| 1995 |

160,630,089.18 |

208,107,597.83 |

118,008,798.14 |

90,098,799.69 |

| 1996 |

208,447,366.59 |

268,839,996.75 |

147,809,112.77 |

121,030,883.98 |

| 1997 |

206,964,002.39 |

264,826,947.48 |

137,801,148.59 |

127,025,798.89 |

| 1998 |

261,474,600.37 |

338,089,113.39 |

161,199,221.52 |

176,889,891.87 |

| 1999 |

246,399,365.04 |

304,359,148.45 |

147,242,910.37 |

157,116,238.08 |

| 2000 |

284,539,486.41 |

351,117,837.26 |

178,155,783.02 |

172,962,054.24 |

| 2001 |

288,115,584.03 |

355,476,654.80 |

187,356,355.86 |

168,120,298.94 |

| 2002 |

389,316,406.45 |

466,322,546.70 |

270,993,053.05 |

195,329,493.65 |

| 2003 |

421,122,564.54 |

503,555,971.70 |

289,562,110.17 |

213,993,861.53 |

| 2004 |

446,091,697.99 |

524,624,200.57 |

292,832,355.42 |

231,791,845.15 |

| 2005 |

563,933,851.05 |

662,332,295.04 |

389,452,552.35 |

272,879,742.69 |

| 2006 |

583,502,898.84 |

664,049,780.44 |

403,376,321.27 |

260,673,459.17 |

| 2007 |

643,196,028.16 |

730,248,478.73 |

430,963,853.43 |

299,284,625.30 |

| 2008 |

662,028,608.63 |

742,497,640.31 |

436,842,738.01 |

305,654,902.30 |

| 2009 |

647,215,530.81 |

716,176,240.39 |

406,799,999.85 |

309,376,240.54 |

| 2010 |

647,741,696.57 |

713,783,918.11 |

406,332,157.05 |

307,451,761.06 |

| 2011 |

651,021,275.75 |

705,999,346.48 |

400,794,317.28 |

305,205,029.20 |

| 2012 |

662,664,406.12 |

713,486,624.70 |

441,199,667.51 |

272,286,957.19 |

| 2013 |

601,341,536.19 |

644,229,545.02 |

252,300,036.69 |

391,929,508.33 |

| 2014 |

556,236,551.33 |

592,708,607.75 |

213,502,205.38 |

379,206,402.37 |

| |

|

|

|

|

| TOTAL |

10,255,724,710.32 |

11,899,656,731.72 |

6,495,138,113.57 |

5,404,518,618.15 |

| |

|

|

|

|

Throughout the first 20 years of life of the agricultural insurance system, new insurance lines have been gradually introduced. New insurable productions have been included in the existing lines during this period, and all the insurance covers have been introduced, extended and improved in the scope of the system for both agriculture and for livestock breeders.

In the livestock area, mention must be made of the appearance of Bovine Spongiform Encephalopathy (mad cow disease), which notably altered the conditions of livestock farming in general. As a consequence, insurance was created for the removal and destruction of dead animals in the farms, leading in 2002 to a major increase in premiums. Moreover, that year existing lines of insurance were enhanced, as with the cover for damage caused by persistent rain in the cherry (spot or stain), and new lines were introduced such as those for olive and red beet yield and insurance of operation with guarantee of yields for extensive herbaceous crops.

In the 2003 season, contracting rose in general for all lines, notably in such insurance as for yield and for fruit trees. Notable among the improvements in the system has been the extension of cover to virtually all climatic adversities for citrus.

During the following years, contracting volume rose thanks fundamentally to the gradual introduction of insurance for removal and destruction in the various autonomous communities and for different animal species. In addition, in 2004, for the first time, a line was opened up to insure the forestry sector targeting farmland reconverted for forestry. Notable in the livestock sector was the provision to poultry farmers of insurance for poultry operations, especially securing “heat stress”, and the extension of the death guarantee for “any reason” in fattened veal insurance.

In 2008, improvements dominated in the conditions of insurance, e.g. arising from the creation of new insurance formulas for citrus fruit, inclusion of cover for failure to set in the Cáceres cherry, the insurability of saplings in woody production lines and the creation of a pork livestock insurance with cover for accidents and

Aujeszky’s disease.

The next major change to the system was the introduction of the management system known as “increasing insurance”, more flexible in contracting, offering the insured party more customised treatment and the possibility of extending the guarantees on the base of fundamental cover for operation. The system also made developments in Agroseguro’s internal management far more flexible, facilitating changes and adaptations as they became necessary. This began to be introduced in mid-2011 and was completed for all agricultural insurance during 2012. The new way of managing insurance, responding to the system’s need to maintain its capacity to adapt to the volume it had reached after 35 years, introduced significant modifications. In general, in connection with producers, the following were the new management system’s aims:

- For all crops, to make it possible to take basic protection against all disaster risks occurring in the operation, giving the possibility to choose higher levels of guarantee by selecting different categories of cover.

- To improve, complete and clarify the information provided by the policy, and offer the farmer customised treatment when contracting, introducing comparative programmes. In addition, contractual conditions were simplified and made more consistent, with an index and a structuring into chapters to make them clearer and more understandable.

- To reduce the number of lines of insurance, grouping all those of the same sector into a single line including all productions of the same type, so that modifications and improvements to the insurance could be made more quickly and efficiently, without having to create new lines.

- To ready insurance for the new framework foreseen in the EU, making possible the development of market risks and also taking into account the possibility of adapting the calculation of subsidies to any changes in European Union provisions.

With this new scheme, a producer wishing to take insurance encounters not just a wide variety of covers but also of prices which are easily compared.

Finally, the reduction in 2013 and 2014 in the development of contracting must be highlighted. It was a direct consequence of adjustments, forced by the economic situation, in the Public Administrations’ budgets to subsidise farmers’ and livestock breeders’ premiums. In fact, as early as 2012, some regional governments forewent the application of subsidies, and ENESA applied the first cuts in subsidy percentages (which in turn provoked regional cuts when their subsidies were referenced to those of the Central Administration). In 2013, ENESA budget cuts were larger, although the Ministry’s notable efforts were responsible for a partial recovery by year’s end. Finally, ENESA’s 2014 and 2015 budget held, so that subsidy percentages could be raised.

Thus the average percentage of subsidy (the Central and Regional Administrations together) moved from 55.41% in 2011 to 39.17% in 2014. The immediate effect was a significant increase of the part of the premium paid by the farmer, and therefore a notable reduction in the volume of premiums which does however have a very positive reading, as the number of policies remained unchanged (around 490,000) as did the area insured (nearly 6 million ha), showing that farmers and livestock breeders continued to confide in the agricultural insurance system, that it is necessary to them, even though they may have decided to take simpler, cheaper covers.

Agroseguro reacted to this situation with a drive to revise cover options to facilitate contracting by developing lower-cost products, while adjusting both technical margins – reducing risk premiums where the loss rate allows that, plus safety surcharges – and charges – revising those for appraisal and commercialisation – raising discounts and facilitating premium payments by instalment. These measures, while unable to fully offset farmers’ increased charges, led to major average reductions in rates in the most important sectors: 5.7% in fruit trees, 10.9% for herbaceous crops and 9.2% in wine grapes.

4. The structure of agricultural insurance

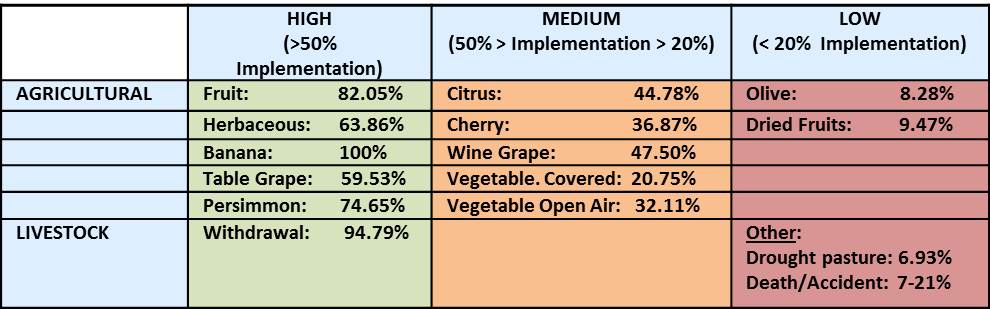

Although as shown above the agricultural insurance system in Spain covers virtually all productions for the generality of the risks affecting them, the degree to which the various lines of insurance are implemented, and their relative importance, differ significantly depending on the productions.

Thus a clear distinction can be made between three groups of production in terms of the degree of implementation: high (more than 50%), medium (20% - 50%) and low (less than 20%). The following table shows the situation in 2014:

While in some cases the reasons for the low level of implementation are very specific (notably the olive, given its importance to Spanish agriculture and of which Spain is by far the world’s top producer and which, in general terms, is characterised by a low sensation of risk in the largest producing regions), the foregoing shows that the continuing margin of growth for agricultural insurance remains highly significant, particularly given the relevance of production in medium implementation.

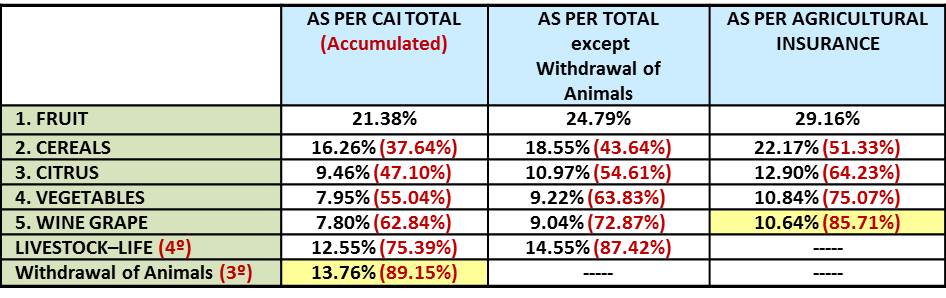

On the other hand, it also proves most interesting to highlight the relative importance of each production sector which, naturally, is in line with their weight in Spanish agriculture. Expressed as a percentage of total premiums, the situation in the 2014 season was as follows:

Various aspects can be emphasised from the above table:

- Fruit tree insurance is clearly that with most weight in agricultural insurance, representing more than a fifth of the system as a whole and nearly 30% of all agricultural insurance.

- The top five agricultural productions exceed 85% of the weight of all non-livestock lines.

- If those five lines are added to insurance for livestock disease and for carcass removal, the total reaches 90% of agricultural insurance.

- By volume of premiums, insurance for the removal and destruction of dead animals from operations is third in overall agricultural insurance

5. Valuations and trends in the loss rate and results in agricultural insurance

a.- Loss adjustment

The moment of the assessment of a loss is what illustrates the usefulness of insurance as a means to cover the damage caused by an unforeseen event. This assessment is done by an expert appraiser, a figure which has evolved technically, structurally and professionally with its increased involvement in the system as a whole.

The process of notification, assessment and payment of the loss is indeed key to the aim of service quality which has always defined Agroseguro, a process which is especially intricate in this sector of insurance, not just because of the intrinsic complexity of cover and appraisal, but also because a massive inrush of claims must be dealt with in short spaces of time. Moreover, in most cases, immediate inspections have to be carried out on dates close to the loss which must then be followed by final assessment as the harvest date nears, doubling the work compared with that in other areas of insurance.

This means that the effort in this respect has been very considerable and has, in recent times, sought to include new technologies in the work of appraisal. At present, assessment generally uses a computer tool – a digital display (

tablet PC) – where the expert notes the results of the assessment and which are necessary in valuing a loss, and enters the insured party’s signature, sending this information to Agroseguro on-line, speeding up claim management and receipt of the indemnification. The insured party receives a mobile telephone message confirming reception, so that immediate information is received at the moment when the formalities for their claim begin.

Much progress has been made in the processing, and indemnification is always paid within the deadlines established in the General Conditions of the insurance. The indemnification deadline is always less than 60 days following harvest or the end of the guarantees.

Agroseguro’s territorial Directors coordinate the activity of these professionals in each area of work and who may be called to zones other than their own when circumstances demand. This capillary structure makes it possible to provide rapid service to those insured in the place where needed because of the seriousness of the situation caused by the loss.

During these years, the number of professionals forming part of the appraisal network has risen from 87 in 1980 to 513 today.

b.- The loss ratio

One of the most significant changes in the number of losses declared was, according to the data, a consequence of the startup in 2001 of lines of insurance for the removal and destruction of dead animals from operations (R&D). During those first years, these lines incorporated more and more animal species into their covers, while extending the scope of application to more Autonomous Communities. This situation, plus the fact that each application for removal was treated as a loss led to an exponential rise in the number of claims during the first years of R&D insurance. As the introduction of these lines has stabilised, so has the number of claims declared.

The situation is the same for the loss rate payable to those insured. Because of the very characteristics of livestock insurance, it is usual for trends in the animal loss rate to match those in contracting.

EVOLUTION OF THE LOSS EXPERIENCE. VALUE IN MILLIONS OF EUROS

| Year |

Agriculture |

Livestock |

Aquaculture |

R & D |

Total |

| 1980 |

0.23 |

|

|

|

0.23 |

| 1981 |

9.22 |

|

|

|

9.22 |

| 1982 |

20.01 |

0.03 |

|

|

20.04 |

| 1983 |

49.12 |

0.05 |

|

|

49.17 |

| 1984 |

78.13 |

0.65 |

|

|

78.78 |

| 1985 |

86.71 |

0.5 |

|

|

87.21 |

| 1986 |

100.15 |

0.29 |

|

|

100.44 |

| 1987 |

72.61 |

0.19 |

|

|

72.80 |

| 1988 |

67.74 |

0.25 |

|

|

67.99 |

| 1989 |

115.58 |

0.33 |

|

|

115.91 |

| 1990 |

134.65 |

0.96 |

|

|

135.61 |

| 1991 |

159.72 |

1.44 |

|

|

161.16 |

| 1992 |

258.73 |

3.34 |

|

|

262.07 |

| 1993 |

132.00 |

5.4 |

|

|

137.40 |

| 1994 |

149.96 |

7.87 |

|

|

157.83 |

| 1995 |

219.04 |

11.55 |

|

|

230.59 |

| 1996 |

70.14 |

16.16 |

|

|

86.30 |

| 1997 |

169.89 |

19.35 |

|

|

189.24 |

| 1998 |

127.84 |

23.8 |

|

|

151.64 |

| 1999 |

284.71 |

28.02 |

0.25 |

|

312.98 |

| 2000 |

122.07 |

41.33 |

0.01 |

|

163.41 |

| 2001 |

242.53 |

47.44 |

3.82 |

0.44 |

294.23 |

| 2002 |

249.34 |

54.93 |

0.98 |

40.02 |

345.27 |

| 2003 |

160.46 |

50.80 |

2.38 |

58.03 |

271.67 |

| 2004 |

259.31 |

44.03 |

5.30 |

70.26 |

378.90 |

| 2005 |

395.31 |

110.02 |

0.03 |

89.56 |

594.92 |

| 2006 |

255.40 |

45.26 |

0.10 |

117.70 |

418.46 |

| 2007 |

279.70 |

43.96 |

0.01 |

135.41 |

459.08 |

| 2008 |

333.28 |

49.57 |

3.44 |

138.41 |

524.69 |

| 2009 |

352.62 |

66.83 |

3.91 |

133.21 |

556.57 |

| 2010 |

372.61 |

55.40 |

0.69 |

131.56 |

560.26 |

| 2011 |

334.10 |

62.53 |

0.09 |

114.46 |

511.18 |

| 2012 |

562.83 |

98.52 |

5.11 |

101.99 |

768.45 |

| 2013 |

366.89 |

60.59 |

3.65 |

85.74 |

516.87 |

| 2014 |

380.44 |

55.26 |

0.21 |

74.68 |

510.59 |

Even so, there are exceptions. In some years the loss rate spikes independently of the contracting volume, for example in 2005, 2009 and 2012, when severe drought caused a sharp rise in the loss rate registered in insurance covering loss for lack of pasture. In aquaculture, peaks in the loss rate are usually linked to periodic ocean storms.

For its part, the loss rate in agricultural lines illustrates the hazard and variability of the risks covered. This was seen in the extremely low loss rate registered in 1996, in the “normal” volume of 2004 and the period 2006-2011 and in the historic high recorded in 2012, when a string of adverse climatic phenomena and in particular a major drought which lasted the whole year raised the loss rate to 768.45 billion euros. 2013 and 2014 saw a return to figures closer to the normal levels of previous years.

The loss rate at the close of the 2014 financial year amounted to 510.6 billion euros, for more than 1,265,000 claims. Of note, given the loss rate volume registered, was insurance for extensive herbaceous crop operations, at 88.48 million euros; olive, with more than 65.81 million; fruits, more than 69 million; or citrus, with more than 55.74 million, among others.

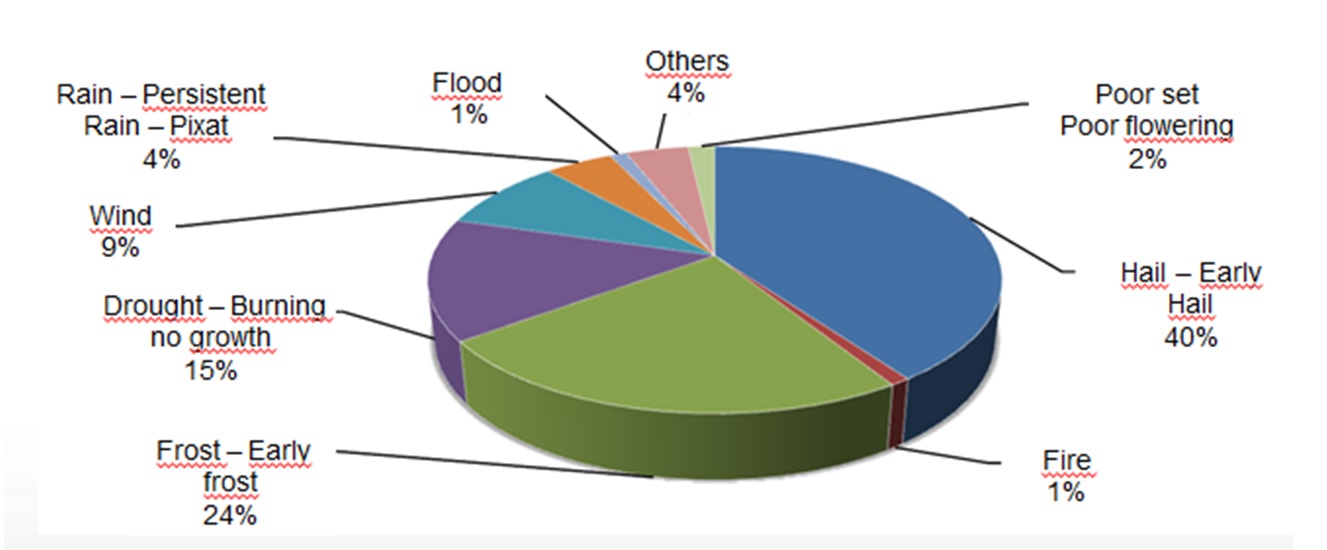

Distribution of the number of agricultural claims by risk (1980-2014)

Distribution of the number of agricultural claims by risk (1980-2014)Hail is unquestionably the risk with the greatest percentage of claims, present from the inception of the system and in all agricultural insurance lines, while also a risk which is constantly present in mainland Spain’s weather.

Frost and drought risks have been covered practically throughout the historical series but it is also the case that these covers are not found in all insurance lines, which explains the lower number of claims compared with hail. However, these are risks whose disastrous potential is much greater, because of their general geographical spread.

c.- The results

As already repeatedly indicated, a characteristic of risks covered in agricultural insurance, given their direct relation with weather phenomena of potentially catastrophic nature, is their extreme volatility, generating a loss rate which varies greatly depending on weather trends and therefore whose technical results also have a “sawtooth” profile. However, overall among the risks covered, three major groups of risk can be made out, given their intrinsic differences – fundamentally their level of hazard – which have therefore different insurance and reinsurance treatment, and which very generically are as follows:

- GROUP A. “Experimental Lines”: particularly hazardous, such as those covering risks which, given their general and intense nature, are more likely to occur with catastrophic connotations, e.g. frost or drought. In technical terms, their cycle and so their actuarial treatment is more than one year.

- GROUP B. “Viable Lines”: covering risks less likely to experience an accumulation of claims causing catastrophic damage, e.g. hail or fire, whose occurrence is more localised. These are susceptible to normal actuarial treatment because, although differing and diverging from year to year, their maximum loss potential is lower.

- GROUP C. R&D Insurance (Removal and Destruction of animal carcasses from operations): fundamentally insurance for “service rendered”, specifically elimination of remains, and demanding a particular infrastructure. Unlike the two previous categories, this insurance usually performs very stably and evenly.

Analysis of the technical results, jointly and for each of these groups, is based on trends in the loss-rate/premiums ratio. The notion of the “loss rate” includes both the indemnifications and the costs for claim handling and loss assessment. The concept of “premium” includes the part intended to deal with the loss rate and its deviations, which is the so-called loaded risk premium.

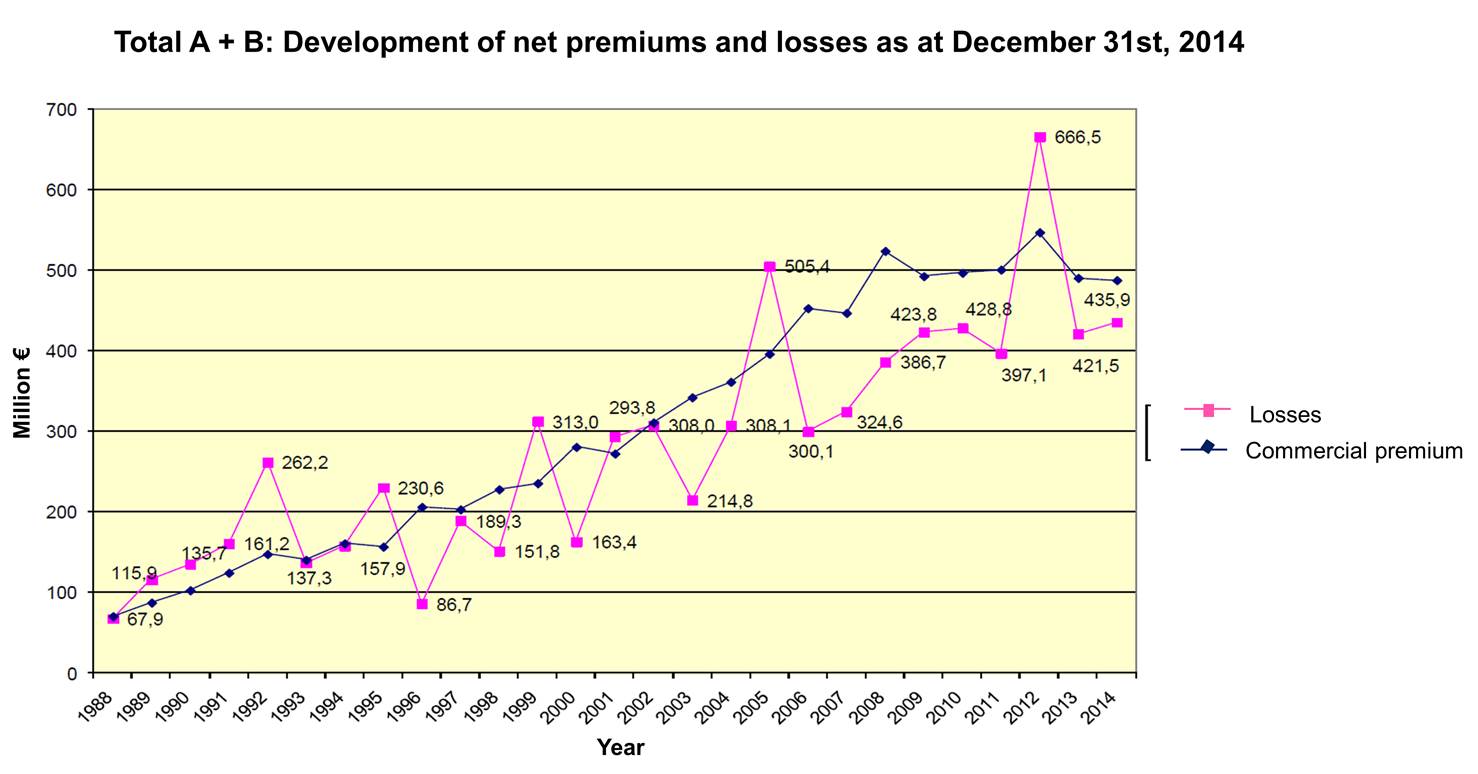

In simplified form, and referred to insurance in the first two groups, the following is a graphic comparison of their loss rates and total premiums:

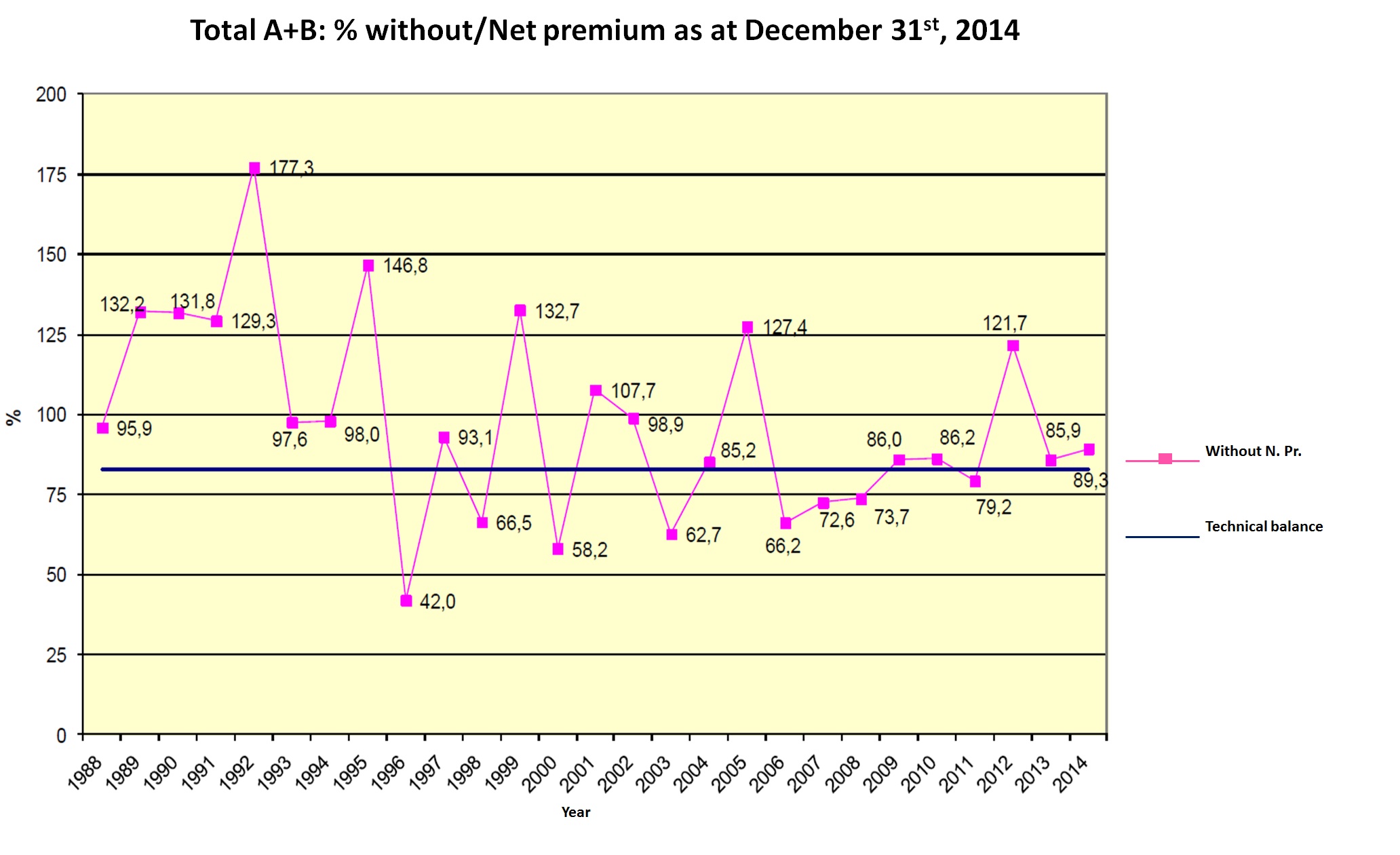

This makes clear the different patterns for total premiums, reasonably stable, and for the loss rate, which is much more erratic. As pointed out however, the loss rate should not be compared with total premiums but rather with the risk premiums. In that case, on the base of 100, showing the risk premiums with a horizontal blue line (representing the technical balance if they coincide with the loss rate), the graphic representation would be:

The conclusion that can be drawn is consistent with the nature of the risks covered: the loss rate varies enormously and spreads around the mean values, with that same effect on results, making the twin safety mechanism essential, i.e. the Equalization Reserve and the public reinsurance system. As a sub-section to this conclusion, it is also notable how the line of trends lies very close to that of the balance on the viable lines (group B), but not on the experimental lines (group A).

For those reasons, the individual result in a given year is not significant and an analysis must be made of much broader historical series if valid conclusions are to be drawn. What in short is important is the long-term trend and here the margin obtained by insurance companies as a whole in 1988-2013 turns out to be 2.4% of premiums, below that registered for general insurance other than life insurance. That same margin, in an analysis limited to the period 2009-2013, more representative of the recent situation, falls to 1.05% of premiums. Thus it is true that, with the risk taken on by insurers limited by a resilient reinsurance system, profit margins must take account of this peculiarity, while it is also a fact that results in the insurance field are extremely tight.

6. The new formulation of agricultural insurance premiums

On 31 January 2013, the then National Competition Commission (now the National Markets and Competition Commission, CNMC) opened an investigation into the combined agricultural insurance system and the organisation and functioning of Agroseguro, which concluded on 25 October that same year with a

“Note on the system of combined agricultural insurance in Spain and its adjustment to the rules protecting competition”. The Note closed the investigations and initiated no penalty procedures, while drawing up some “recommendations from the perspective of defence of competition” which referred to three aspects:

a.- An overall review of the agricultural insurance system

The CNMC accepts that agricultural risks, given their natural origins, high degree of exposure and catastrophic potential, raise greater technical difficulties for their insurance by private companies than those encountered by other economic sectors, to the point where cover by individual insurance institutions is not viable, and it concludes that, after more than 30 years, and considering the progress of the Spanish economy in general since then and, in particular, the level to which the Spanish insurance sector has developed, it would be advisable to review whether a system of agricultural coinsurance continues to be justified.

The analysis suggested by CNMC was commissioned from an independent firm specialised in the matter, which ended it with a report according to whose conclusions agricultural production is, relative to the risks which it must bear, affected by a significant systemic component with a lack of sufficient independence among risks, leading to correlation of individual farmers’ outputs, which limits the capacity of the private insurance sector to maintain adequate reserves, and sufficient access to reinsurance to cover these risks, and for relevant problems of adverse selection. All that, together with conditioning factors imposed by the regulatory framework for this insurance (the breadth of the portfolio of productions and risks that must be covered in combined form; insurance companies’ obligation to subscribe cover for any farmer and livestock breeder who applies for it, with no possibility for selection), and also based on international experience and the development of agricultural insurance itself in Spain, leads to the conclusion that the incentives for private insurers to provide agricultural insurance with current covers would be limited, and allows the coinsurance system to overcome these limitations and take up risks individual insurance institutions would not cover.

b.- Elimination of limits on competition between institutions

A second group of recommendations refers to the elimination of certain limits, in particular:

- The limitation of maximum participation in coinsurance tables, fixed at 25%. The insurers’ efficiency, reflected in the contribution of a greater volume of premiums to the system, should not be discouraged with maximum limits, provided that this does not contravene the legislation on the protection of competition.

- The minimum 0.05% participation in coinsurance tables, even though an institution’s contribution is systematically below that figure, or zero. No justification is found for participation, however small, for those not contributing premiums. It is thus recommended that this lower limit be eliminated.

In both cases, the Agroseguro’s Board of Directors, meeting on 19 December 2013, resolved to eliminate the limits immediately.

c.- Premium calculation

The CNMC considers that the coinsurer entities who are AGROSEGURO, S.A.’s shareholders could compete at least in three areas: client capture, the quality and variety of services (consultancy, speed, etc.) and prices (the more efficient they are, the better the rates they can offer). So while these differences do occur in the first two cases, in relation to the third the CNMC admits that, as the institutions coincide, in identical contractual conditions, to cover the same risks, it is justified for risk tariffs (aligned to the loss rate) to be based on common statistics, like the consideration of a single surcharge to meet costs which are also common (fundamentally arising from Agroseguro’s management on behalf of all the institutions), while considering that it might be that the final premium offered by each insurer should be formed by adding to the above the surcharge for specific administration or commercialisation charges met by each participant, so that the most efficient can offer better prices.

At the same time, and also throughout 2013, an Inspection was run in Agroseguro by the Directorate-General for Insurance and Pension Funds, which ended with a requirement which also affected the formulation of the premium, and stated that the reinsurance premium charged by the Consorcio de Compensación de Seguros, until then formulated as a surcharge external to the commercial premium, should form a part of it – and, more specifically, of the risk premium – in this way integrating the base for calculating the provision for unearned premiums on 31 December each year.

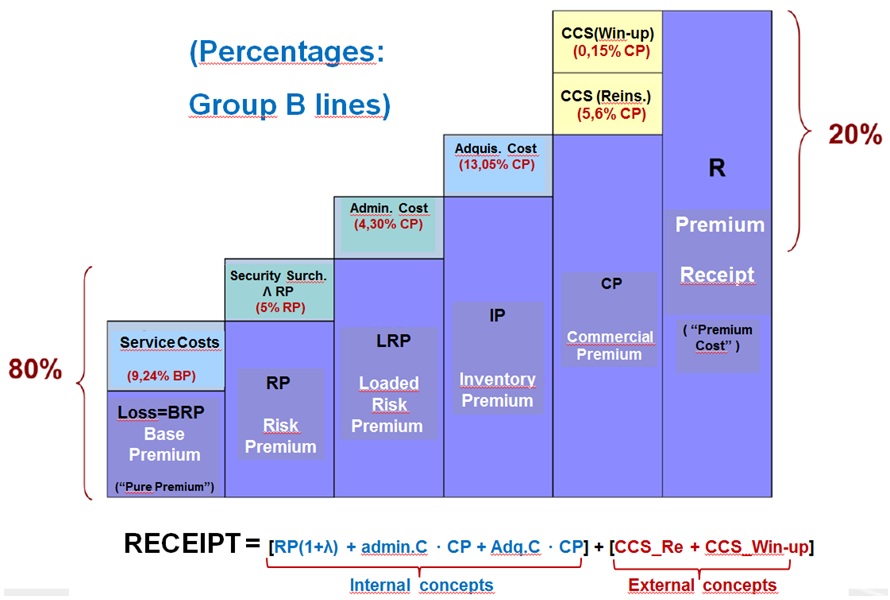

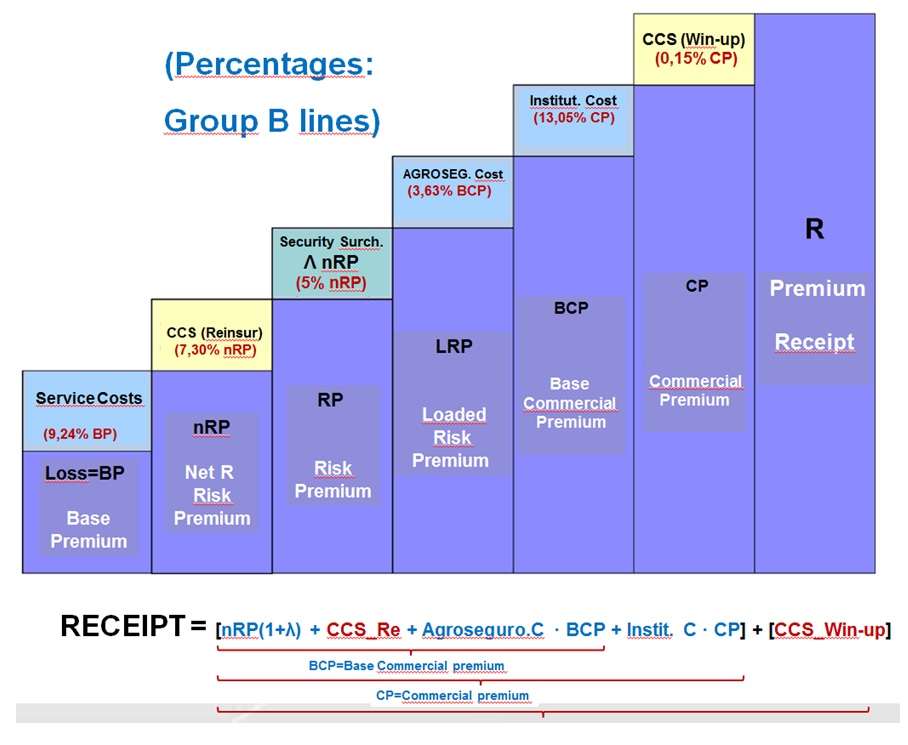

The technical bases of agricultural insurance require the price of the insurance to be formulated on the basis of the definition of the Pure Premium and the application to it (the excesses discounted) of surcharge coefficients to cover each of the expense items (administration and acquisition), until reaching the Commercial Premium.

As explained, in connection with the Commercial Premium, to obtain the Premium Receipt – the end cost of the insurance – the reinsurance surcharge in the Consortium’s favour and the surcharge for the Consortium’s winding-up activity were applied.

Following the notation of the technical bases, the rate is formulated so that the commercial premiums are calculated from the Loaded Risk Premium, applying the management costs, differentiating them according to their use (administration and acquisition – commercialisation). Thus, the way in which the final cost was traditionally formed was, graphically speaking:

As a result of the CNMC’s recommendations (consideration of the common costs on the one hand and the individual costs of each institution on the other) and the DGSFP’s requirements (to integrate the Consortium’s premiums into the premium rather than specifying them in the receipt) the composition of the premiums was reformulated, with the application of two modifications:

- To include the Consortium’s reinsurance premium in the risk premium and to reformulate the coefficients so that the figures (in €) for management costs and the total premium are the same as with the formulation in the 2014 Plan.

- On the basis that the Consortium’s reinsurance forms part of the risk premium, to formulate a base Commercial Premium for Coinsurance which includes Agroseguro’s costs (common to all the coinsurers) but not the coinsurers’ charges. The Commercial Premium (total or final) would be the sum of the base Commercial Premium (the same for all coinsurance) plus each coinsurer’s management costs.

In other words, graphically:

This new formulation of premiums, completing compliance with the CNMC’s recommendations and the DGSFP’s requirements, began to be applied to agricultural insurance in the 2015 Plan.

7. Conclusions

By way of brief conclusions, the following can be highlighted:

- Risks affecting agriculture are, given their link to the weather, very high, so that farmers and livestock breeders need a cover mechanism backed by the Public Administrations. Insurance is the best alternative, for both agriculture and livestock entrepreneurs, who receive a universal guarantee – from which no producer can be excluded – and indemnification proportional to the loss suffered, and in a short period, and for the Public Administrations who thus have a tool enabling them to budget a priori, which is less costly (in terms both of the technical valuation of the damage and of the cofinancing charged to the farmer) and more equitable, also allowing them to adopt certain agricultural policy measures.

- As to the specific insurance mechanisms, the nature of the risk –catastrophic potential and extreme volatility, together with the impossibility of risk selection – make the following necessary from the standpoint of insurance technique:

- Coinsurance cover, enjoying greater synergies the larger the insurer grouping.

- The creation of equalization reserves to meet major and frequent loss rate deviations.

- A reinsurance mechanism which protects the system financially in exceptional situations and which is stable medium- and long-term. The public nature of the reinsurer is, for many reasons, more than justified.

- Subsidies for insurance costs are indispensable. The Public Administrations, both central and regional, are fully aware of that and although they have had to weather budget difficulties they back the insurance system unreservedly.

Both the organisation and operation of the Spanish agricultural insurance system is today fully consolidated, and European regulation of competition and state aid is a guarantee of continuity.