Spain is a country particularly prone to suffering floods and its agriculture is an especially vulnerable sector. In fact, the climate swings we face, together with the country’s orography and the structure of agricultural holdings and production, mean that Spanish agriculture is highly sensitive to this risk. Moreover, in the context of increasingly evident climate change, a trend towards the occurrence of ever more extreme phenomena is taking hold and flooding is sure to become one of the most common manifestations of this.

Floods are generally caused by two separate factors in Spain:

Torrential rains within a very short space of time. These are so-called cut-off lows, more widely known as gota fría in Spain. Above all, they occur on the Mediterranean coast and in inland zones, and the risk of them is particularly high in late summer.

Rapid thawing of snow built up in winter, mainly in the Ebro valley.

Floods attributable to either of these two phenomena are potentially hazardous but, due to the rapidity with which they appear and the intensity that they can attain, cut-off low events are perhaps more destructive.

The damage which they prompt affects both rural areas and urban zones. In the countryside, farmers usually look on helplessly as they lose their crops or the infrastructure on their farmsteads, experience an inability to venture onto their pieces of land to apply necessary remedies, or witness how diseases linked to dampness and crops progress proliferate. And this happens both in zones neighbouring fertile river plains as a result of overflows and in another sort of areas on account of torrential rains.

We are consequently up against a persistent risk in Spain, where there are zones with a high probability of this occurring and harming the countryside, to which farmers can do little or nothing about. The high level of recurrence and the destructive potential mean that it is hard for the individual private insurance initiative to offer cover at an affordable price. This is why, as a system bringing together the public interest and private management, agricultural insurance is the most reliable way to take on this risk.

II. Including and identifying the risk in the agricultural insurance system and how it works

a) The introduction of flood risk in agricultural insurance

As a basic means of managing risks on farms, there is the so-called Combined Agricultural Insurance system, which is regulated by Law 87/1978, in turn implemented through the regulations approved by Royal Decree 2329/1979, which is substantiated in the annual agricultural insurance plans approved by the government at the suggestion of the State Agricultural Insurance Agency (Entidad Estatal de Seguros Agrarios, ENESA), which is a body under the Ministry of Agriculture, Fisheries and Foods, that draws up these plans in conjunction with the Ministry of Economy and Business (Directorate General for Insurance and Pension Funds and Consorcio de Compensación de Seguros), and under professional agricultural organisations, agriculture and food cooperatives, and the insurance industry, represented by Agroseguro.

Since its inception, the core aim of this insurance system in Spain is to universalise agricultural sector cover against adverse weather conditions and other uncontrollable natural phenomena. In consonance with this goal, in our agricultural insurance model, all production is insurable and all sorts of risk can be insured against. Even so, including a crop or a risk as insurable in the annual agricultural insurance plans is conditional upon ENESA carrying out the relevant technical and financial feasibility study beforehand.

Given its particular significance, the risk of flooding was considered with the aim being that any insured production should have coverage for any damage caused, irrespective of the type of policy taken out and the geographical area. This meant including basic cover in all policies, which should come at a reasonable cost that farmers could afford. To this end, the corresponding initial feasibility study was conducted, which took into account statistical data sets from 1969 to 1997, including meteorological data, information on floods, damage recorded at municipal level and how the risk affected the various different crop types.

As is only to be expected, for flood cover to be feasible, it was necessary to apply a correct rating ensuring that the amount collected from premiums was enough to provide for the loss rate that might occur. It was essential to measure the risk level very well and to propose the basic premiums to apply. For this purpose and using the information analysed, the Peninsula was carved up into seven zones which were assigned an equivalent risk level and a benchmark rate (rates in percentage terms), as the table below shows:

Risk zone

Benchmark rate

I

0.30

II

0.35

III

0.45

IV

0.55

V

0.70

VI

0.85

VII

1.00

Table 1. Benchmark rates in risk areas.

Source: Own research.

After measuring the risk level, the effects of the flooding/torrential rain had to be adjusted for the specific circumstances of each crop by obtaining a factor to apply to each of them. The factor calculated for each crop according to its sensitivity to flood risk was thus:

Crop

Factor

Grain legumes

0.40

Cereals

0.50

Fruit

0.80

Olives

0.80

Wine grapes

0.80

Fodder crops

1.00

Industrial crops

1.20

Citric crops

1.40

Table grapes

1.40

Vegetable and flowers

1.50

Table 2. Factor for calculating the premium rate per crop.

Source: Own research.

This factor, together with the zone rate, is what determines the premium that is appropriate for each crop in each district, according to types, options and products insurable, for each line of insurance. In other words, to obtain the basic premium for floods/torrential rain for each region and crop, the benchmark rate for the relevant zone (Table 1) should be multiplied by the crop factor (Table 2).

The aforementioned study brought about the Agricultural Insurance Plan for 1998, which was approved under a cabinet resolution of 28 November 1997 and included the risk of flood/torrential rain for all crops and in all lines of insurance.

With regard to the definition of the risk covered, this was done through referring to the damage occasioned, meaning that caused by downfalls triggering overflowing of rivers, sea inlets, streams, watercourses, lakes and lagoons, that originates currents which sweep away objects, river surges and spates. They must also produce certain self-evident effects in the zone where the plot of land is located (property being carried away, items being covered in mud…). The loss event must leave obvious signs of flooding on the plot of land and in its surrounding area.

After the occurrence of the loss event has been accepted, losses are covered that relate to the waterlogging of roots, items being caked in mud, the physical impossibility of harvesting throughout the event or the 10 days afterwards and blight and diseases that appear throughout the event or within the 10 days subsequently due to the physical impossibility of applying appropriate remedies, whenever this is as a result of the loss event.

Nowadays, flood/torrential rain cover is included in all policies and covers losses not just of crops, but also of planted items due to the death of trees or seedlings. Furthermore, if the appropriate cover has been chosen, losses involving facilities are also insured (greenhouses, vine arbours, trellises and espaliers, and irrigation equipment).

The table below shows the current conditions for coverage:

MODULE 1

MODULE 2

MODULES 3 and P

CROPS

Sum insured

100%

100%

100%

Indemnity

Per farm

Per farm/plot of land

Per plot of land

Deductible

20%-30%

20%

20%

PLANTATION

Sum insured

100%

100%

100%

Indemnity

Per farm

Per farm/plot of land

Per plot of land

Deductible

20%-30%

20%-30%

20%

FACILITIES

Sum insured

100%

100%

100%

Indemnity

Per plot of land

Per plot of land

Per plot of land

Deductible

Without a deductible

Without a deductible

Without a deductible

Table 3. Conditions for coverage of flood/torrential rain risk.

Source: Own research.

b) Experience of the functioning of the coverage

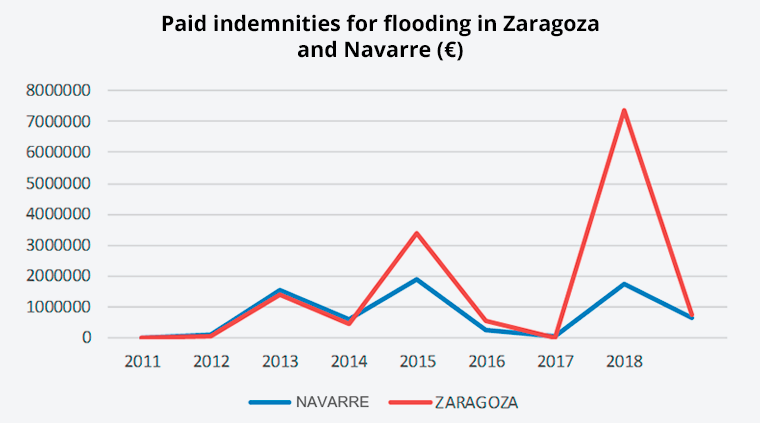

The experience acquired by the agricultural insurance system with respect to covering flood risk has shown that it is feasible and sustainable and that the insurance has worked and adjusted indemnity to actual losses in agricultural production. Particularly in recent years, there was an unbroken chain of flood/torrential rain phenomena. We experienced loss events due to cut-off lows, such as those which took place in the 2012, 2016, 2018 and 2019 seasons on the East of Spain (Levante), and phenomena involving rivers overflowing due to torrential rains at their head or exceptionally fast thawing of snow in the Pyrenees, such as the overflowing of the river Ebro in 2013, 2015 and 2018. As regards the latter, it can be seen in Figure 1 how compensation was paid in keeping with the severity of overflows, which indicates a marked upward trend.

Figure 1. Indemnities for flooding in Zaragoza and Navarre.

Source: Own research.

Given these developments, premiums for flood risk have managed to bear this loss rate well. The 2019 cut-off low event which we have just suffered was of such a magnitude that, in all likelihood, it will mean a greater volume of indemnity than was associated with all previous events; yet, even in these circumstances, the insurance policy has proved to be fit for its purpose and risk cover to be adequate.

III. The case of the cut-off low of september 2019

a) Description

In mid September 2019, there was an episode of torrential rains in Spain which AEMET (the State Meteorological Agency) classified as a cut-off low (closed upper-level low in the atmosphere), which exhibited record features judging by the severity of the destructive effects it originated. The high damage levels which this phenomenon led to were due to a mix of the following factors:

Unusually heavy torrential rains.

The overflowing of rivers, watercourses and streams.

The vastness of the affected area.

The fact that it lasted for several days.

Storms with hail.

The combination of all of these factors, together with the orography characteristic of the worst-affected zones, with mountains very close to the sea which curb cloud movement, caused a great deal of destruction to be recorded, both in the countryside (crops and facilities) and in urban areas, and even the loss of human lives.

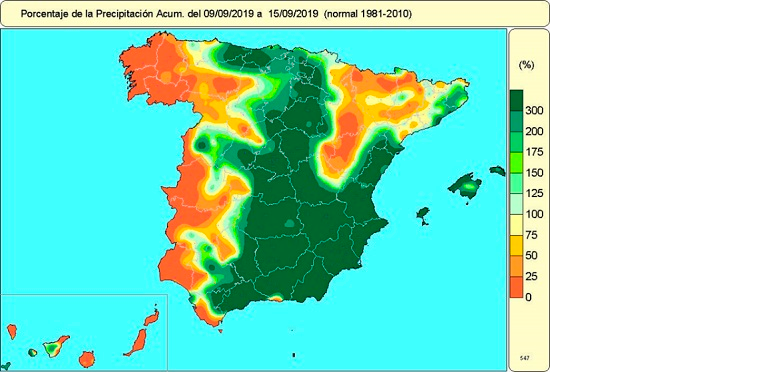

Figure 2 depicts the percentage of accumulated rainfall in the Peninsula from 9 to 15 September 2019 (where 100% is the average rainfall for the 1981-2010 period), illustrates the extraordinarily large area which this event managed to affect:

Figure 2. Percentage of accumulated rainfall from 9 September to 15 September with respect to the 1981-2010 mean.

Source: AEMET.

The situation was exceptional in La Vega Baja del Segura, where it had been unprecedented in the past 100 years. In only a few hours, an amount of rain equal to the fall for a whole year collected, giving rise to huge flood.

Photograph 1. Flooding in La Vega Baja del Segura.

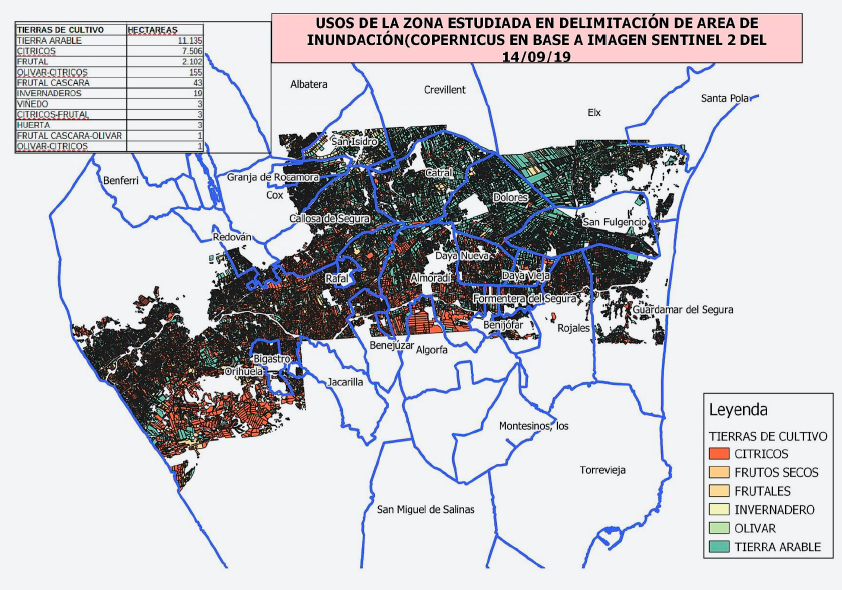

The wide area flooded is of great agricultural significance, a substantial number of crops being hit there and of high economic worth besides.

Figure 3. Delineation of the flood areas. La Vega Baja del Segura.

Source: Regional Department of Agriculture.

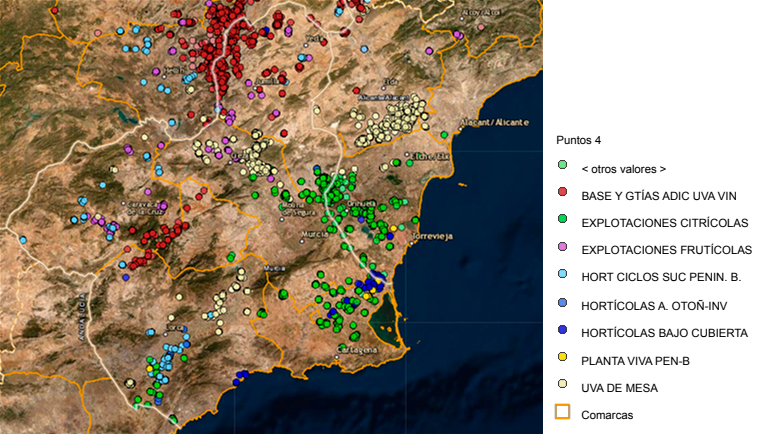

Several weeks after the cut-off low occurred, claim forms are still being received. Figure 4 shows the distribution and high concentration of losses, as well as their location by lines of insurance in the provinces of Albacete, Alicante and Murcia.

Figure 4. Location of claims received.

Source: Own research.

b) Damage to crops, plantations and farming facilities

The range of symptoms of the damage caused by flood/torrential rain loss events in the agricultural sector can be broad depending on the characteristics of the loss event occurring and the crop affected.

Direct loss or damage involving crops and plantations

By way of direct loss or damage in those zones where the water has built up in large amounts and over an extended time-frame, the main symptoms for citric crops and grains were mud-covering, drying out and later defoliation of trees, and the falling of fruit which has remained in contact with the water.

Photograph 2. Citric fruit plantation with defoliation of 90% of trees.

Photograph 3. Marked falling of fruit and drying out of trees.

Other of the crops worst affected by the build-up of water on plots are horticultural produce due to being cultivated flush with the ground. Symptoms here include plant death, burial, covering in mud and carrying-off of fruit, as well as it becoming impossible to gather crops such as melons and watermelons, which will take weeks to get rid of all the accumulated water.

Photograph 4. Waterlogged melon patch.

Other major symptoms observed were the dragging away of branches and other materials covered in mud, even falling over or uprooting of trees and structures due to the force of the spate. In the case of trees where branches and debris accumulated around the lower part, fruit was pierced and grazed, even carried away. Damage also occurred to structures such as vine arbours, for example, to grapes.

Photograph 5. Collapsed vine arbour trained on espalier.

Photograph 6. Plantation against espalier that has been brought down by the force of the water and where the land has been burrowed underneath with exposed roots present.

With the rice crop, the rains prompted seeds to germinate in the case of early varieties such as short-grain Valencia rice, which had started to be harvested.

Photograph 7. Plantation of germinated rice (short-grain Valencia Variety).

On the other hand, with respect to the table grape crop, there was splitting of the fruit, which is known as cracking, followed by grey mould appearing (botrytis).

Photograph 8. Serious damage to table grapes (Sugar Crisp variety).

Indirect loss or damage involving crops and planted items

Besides direct damage or loss, other forms of this occurred on farms which can be described as indirect, which are also covered. Notable here is when it becomes impossible to carry out harvesting within the right time or to apply treatments required for the crop to develop.

Damage to farm facilities

Fences and low walls on farms fell over and there was washing away and vanishing of the arable layer, as well as detaching and dragging off of soil, and build-ups on the plot of all kinds of debris that had been washed along.

Photograph 9. A fallen fence.

Photograph 10. Land carried away and soil lost.

c) Claims handling

In the first month after the cut-off low happened, loss claims were received in relation to 37,869 ha, although they will still arrive beyond this period, on account of, among other things, the developmental nature of damage from the loss event. Shown below is the distribution of claims received per crop:

Crop

Affected area (ha)

Citric crops

9,670

Wine grapes

9,120

Vegetables

6,368

Olives

3,114

Herbaceous plants

2,704

Table grapes

2,444

Nuts and dried fruit

1,922

Other crops

2,527

TOTAL

37,869

Table 4. Affected area per crop.

Figures as of 02/10/2019, own research.

The worst affected areas were Alicante and Murcia, although there was also damage in inland areas in Albacete, Ciudad Real, Cuenca, Granada, Madrid and Zaragoza.

As claim forms come in, tasks are entrusted to freelance professionals who, in suitable numbers, perform appraisal work. Final appraisal is generally carried out for crops due to be harvested imminently or where the damage is to such an extent that this prevents the crop from continuing. For other crops, such as citric fruit, an immediate inspection is made to confirm that damage exists, quantify the losses (damage by amount) as a result of the loss event and the final appraisal is postponed until close to harvesting, when the ultimate damage to holdings is specified.

It is important to point out that, in agricultural insurance, appraisals are conducted pursuant to regulated adjustment rules that are familiar to all agents participating in the insurance, which provides legal security for all the parties in the insurance contract.

The intensive use of technology which Agroseguro has made, both in receiving claims and in handling assignments, and the utilisation of computerised tools such as tablet devices by adjusters, is a huge help towards handling information from the results of appraisals almost in real time, which allows compensation to be paid out within the space of no more than 30 days from when the final appraisal is made.

Quantification of the development of damage from a loss event of this kind becomes necessary over the weeks after it. In the case of the September 2019 cut-off low, as of mid October, the estimate stood at around 84 million euros.

This therefore concerns a loss event of exceptional magnitude that is a one-off but which has come on top of the set of claims in a year that has been characterised by, among other things, a notable lack of rain, and this with one quarter still to go in which there is a considerable volume of crops that are exposed to risk. After two years running which are among the most severe on record for agricultural insurance, it is more than likely that, once again and in view of the potency of this cut-off low, the re-insurance cover provided by the Consorcio de Compensación de Seguros will have to be activated as financial guarantor of last resort in the system. Given the potentially catastrophic nature of the risks that affect agricultural and livestock activity and, by extension, the extremely high volatility of the results, this re-insurance mechanism is the one that endows agricultural insurance with long-term stability.

We can chiefly draw the following general conclusions from what we have discussed:

The risk of flooding from torrential rains is very present in Spain and, due to the substantial damage this causes, including it in the agricultural insurance system is vital for farmers. After appropriate studies were made, this risk was first introduced into agricultural insurance in the plan for 1998 and is today a fundamental item of cover in all lines of agricultural insurance that are included in the system.

The risk has been properly gauged from a technical standpoint and has thus been allocated a premium that is reasonable and affordable for producers.

The coverage works satisfactorily and both addresses the losses which farmers face and strikes a balance between premiums and indemnity.

It is worth noting the potential impact which climate change could be having on this risk, as well as on others that are also included in agricultural insurance and associated with a phenomenon which contrasts with it, i.e. a lack of rain. The most recent manifestation of this is the cut-off low witnessed in the Peninsula in September 2019, regarding which certain conclusions can be drawn:

This cut-off low engendered a loss event extraordinary in its magnitude and which posed a challenge to the system, which responded flexibly and managed to keep cover feasible.

In addition to flooding/torrential rain, the loss and damage that was caused by the passing of this atmospheric depression was also due to persistent rains and hail-storms. Not only did these cause damage to production, but also to plantations and seedlings, as well as to farm premises, mainly involving greenhouses and vine arbours.

The damage to agriculture has been very great, especially in the provinces of Murcia y Alicante. The worst-hit crops are citric fruits, vegetables and grapes, both for wine-making and eating at the table.

The effective handling of the loss event has been enabled thanks to collaboration among all of the agents involved in this insurance. Appraisals are being made at a pace set by the harvesting of the main crops and pay-outs are taking place within minimal time-frames.

The loss and damage varies, from the kind that affects production and the crop itself, which is both direct (hits the crops and planted items themselves) and indirect (related to it becoming impossible to carry out harvesting or necessary to delay it, or preventing the application of treatments), to the sort that is caused to the structural elements that are associated with the plots of land which farms comprise.

In the countryside, farmers usually look on helplessly as they lose their crops or the infrastructure on their farmsteads, experience an inability to venture onto their pieces of land to apply necessary remedies, or witness how diseases linked to dampness and crops progress proliferate. And this happens both in zones neighbouring fertile river plains as a result of overflows and in another sort of areas on account of torrential rains.