Pierre Tinard

Director, Catastrophe Modelling

CCR Re

The extensive eruption of the Cumbre Vieja Volcano in the Canary Islands, at the time of this writing still in progress after many weeks, has raised our awareness that a hazard that may seem tenuous and infrequent can have a huge impact on the insurance industry, destroy hundreds or thousands of properties, disrupt communications and distribution networks, and bring local economic activity to a halt for many months. An event of this type could take place in the territory of France, which harbours some of the most active volcanoes on the planet that have caused tremendous catastrophes in the past. Like Spain, France has established an insurance instrument capable of responding effectively to the need for compensation specific to natural disasters.

The natural catastrophe compensation scheme and the role of the CCR

France is one of a small group of countries with a mechanism that ensures suitable compensation, at affordable rates, for property damage sustained by private individuals, companies, and local government produced by natural disasters. This mechanism is a compensation scheme for natural catastrophes (Nat Cat) that was brought into being by the Act of 13 July 1982. This insurance scheme has proved successful in alleviating a gap in coverage for natural hazards, which had been underinsured until that time.

In practice the insurance scheme takes the form of a public-private partnership. In that legal form the Caisse Centrale de Réassurance [Central Reinsurance Fund], or CCR, is enabled to provide insured parties who are interested in unlimited reinsurance coverage backed by the French government for natural disaster hazards in France. The CCR was established in 1946 and is wholly owned by the Government of France. As a public reinsurer, it supplies the public component in this partnership.

The CCR's area of activity extends beyond the bounds of insurance coverage, by also: (i) bringing financial balance to the natural disaster compensation scheme; (ii) participating in evaluating the financial consequences of natural catastrophes, collecting data on insured property damage, and devising its own modelling tools; and (iii) boosting the prevention of natural perils by providing a knowledge base and key indicators for industry stakeholders.

Operation of the Nat Cat scheme

General principles

In practice, natural disaster insurance is a compulsory extension of coverage for all property insurance policies (multirisk home, all-risk car, commercial premises insurance, etc.) except for marine insurance. Accordingly, insuring property against physical damage (fire, theft, water damage, etc.) is the prerequisite for gaining entitled to compensation.

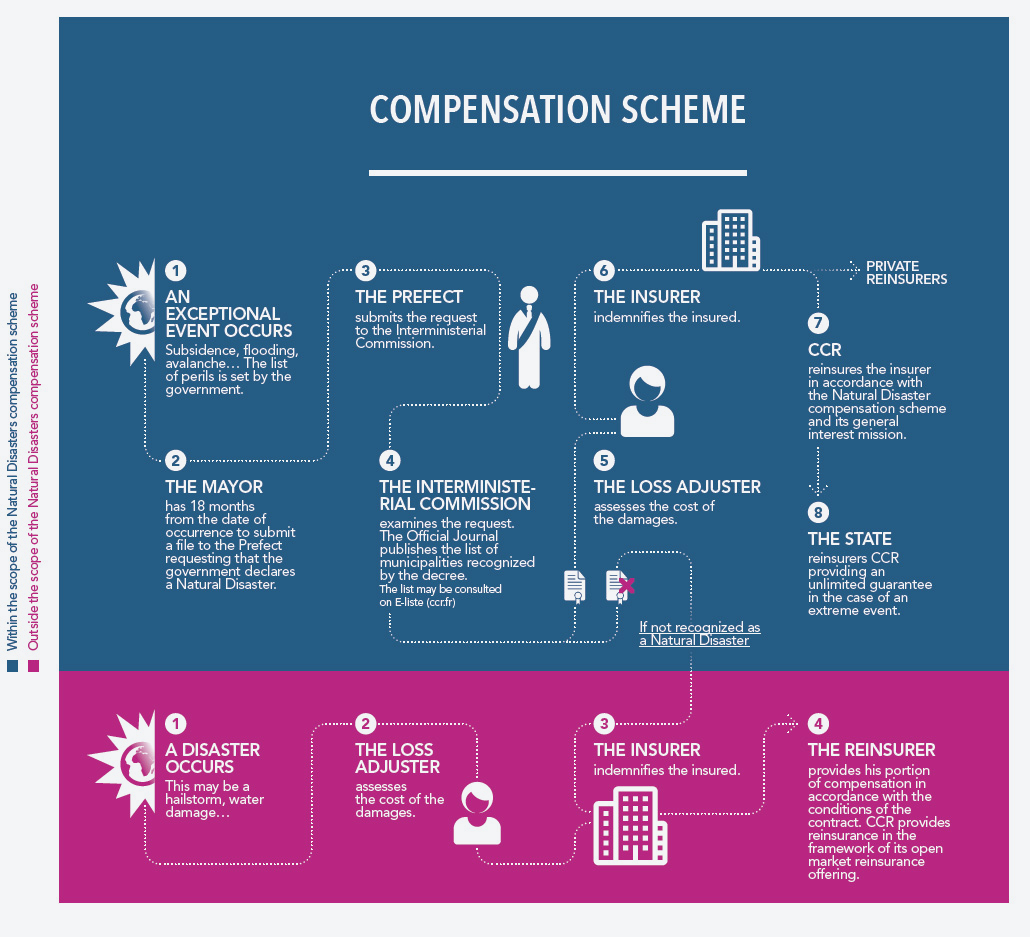

The insured will be compensated for damage caused by a natural catastrophe when the municipal authorities have asked the French government to declare a natural disaster. The government then evaluates those requests based on detailed scientific reports that will show whether the natural event was unusual in its intensity or not (Figure 1). Under this procedure, frequent low-intensity events are excluded, and only events that have the highest impact are covered. The government will then issue an interministerial decree and declare a natural disaster depending on the characteristics of the event, its geographic extent, and the length of time it has lasted.

Figure 1. How the natural catastrophe indemnity scheme operates in France.

Source: CCR, 2021.

Funding for the scheme

The Nat Cat coverage extension requires paying a surcharge on the premium. The surcharge is based on the principle of national solidarity, the cornerstone of the French Constitution, and hence it is the same throughout France, irrespective of the insured property's exposure to natural hazards. The surcharge is set by the French government, and the rate is currently 12% of the premium for the property damage cover under the basic policy for property other than motor vehicles and 6% of the premium for fire and theft coverage for land motor vehicles (or, where there is no such cover, 0.50% of the property damage premium).

In 2020, the cumulative premiums collected under the Nat Cat scheme came to 1,720 million euros for the automobile and property damage lines. Business risks (commerce, industry, agriculture) accounted for some 690 million euros, private property risks (homes) some 910 million euros, and motor vehicles some 110 million euros.

Thus, it is estimated that a business is covered under the Nat Cat scheme for a premium surcharge of around 100 euros a year, a private individual for between 25 and 30 euros a year, and a vehicle for less than 10 euros a year.

Limits of indemnity

By law Nat Cat protection covers "non-insurable direct property damage caused by the unusual intensity of a natural agent where the usual measures taken to prevent such damage could not be taken or would not have prevented the damage from occurring". This applies to an extensive series of natural phenomena including floods, drought, ground movement, storm surges, hurricanes, earthquakes, tsunamis, avalanches, and volcanic eruptions, as well as all of their associated repercussions.

The law stipulates that direct property damage will be covered only if there is coverage under an insurance policy that serves as the basis for the Nat Cat coverage extension. The risks covered are:

direct property damage to buildings, structure and contents, including the replacement value if the policy includes that coverage,

demolition and debris removal expenses for the insured property that has suffered the loss,

damage caused by moisture or condensation from standing water on the property,

the cost of pumping, cleaning, and disinfecting damaged property and salvage measures in general,

the cost of geotechnical studies needed to recover the property that is covered,

vehicles that have own damage insurance (compulsory third-party liability does not cover losses of this kind).

Also covered is business interruption from direct damage where the underlying policy includes this cover.

The law provides for the following deductibles:

€380 for residential properties and motor vehicles,

10% of the loss, with a €1,140 minimum, for business properties,

3 business days, with a €1,140 minimum, for business interruption.

These deductibles may be raised by a factor of from 2 to 4 in case of repeated losses in municipalities that do not have a natural risk prevention plan or based on the number of declarations of natural disasters issued for the same type of natural catastrophe in the five years preceding the date of the latest declaration.

Lastly, it should be pointed out that damage is covered whether it occurs in the territory of metropolitan France or in the overseas territories of Guadeloupe, Martinique, French Guiana, Réunion, Saint Pierre and Miquelon, Mayotte, Saint Barthélemy, Saint Martin, and Wallis and Futuna. Insured property damage in each of these territories will be covered even if the event that causes the damage is located outside France. For instance, an earthquake in Italy that causes damage in Nice, a tidal wave that crosses the Indian Ocean and causes damage in Réunion, or volcanic ashfalls that affect Guadeloupe even if they come from the Soufrière Hills Volcano on the island of Montserrat 80 km distant are indemnifiable if the natural events can be demonstrated to be unusually intense.

Several French overseas territories are active volcanic islands in the Caribbean or in the Indian Ocean and hence are directly exposed to multiple impacts caused by volcanic activity.

Nat Cat losses and extreme events

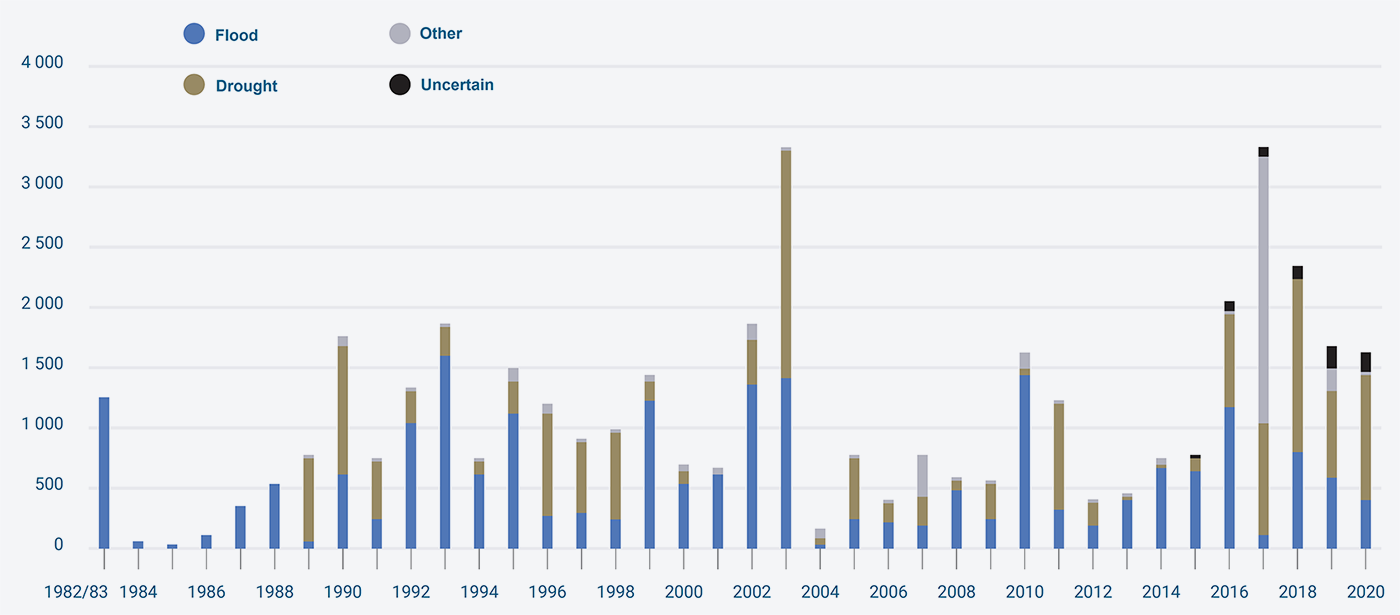

Nat Cat premiums brought in 1,720 million euros in 2020, but losses from natural catastrophes are themselves quite substantial, though subject to interannual variations (Figure 2). Around 41,000 million euros in losses were paid out in the period from 1982 to 2020, that is, mean annual compensation of 1,086 million euros. Some 42 million euros of that was in the motor vehicle line. France is mainly exposed to two recurring natural perils, floods, which account for around 53% of cumulative losses, and drought (clay soil contraction and expansion), which account for 37% of losses. The other perils account for the remaining 10%.

Figure 2. Nat Cat loss rate, property damage from 1982 to 2020.

Source: CCR, 2021.

The most recent of the chief significant events over the history of the scheme is unquestionably Hurricane Irma, which occurred in 2017 and swept across the islands in the French Antilles, producing insured damage totalling on the order of 2,000 million euros, substantially higher than that year's Nat Cat premiums. Other events also took place in that same year, particularly an intense drought that caused some 800 million euros in losses. Another year, 2003, was also a year of record losses amounting to 3,300 million euros, including over 1,500 million euros from drought and close to 1,000 million euros from a major flooding event.

Apart from the observed losses, in the CCR's estimation there are other probable extreme events, such as flooding in Paris and the surrounding region, that could produce losses ranging between 16,000 and 28,000 million euros, or an earthquake near Nice in southern France, whose cost could come to between 9,000 and 13,000 million euros.

Volcanic eruptions and France's Nat Cat scheme

Despite the fact that French territory, its overseas territories in particular, are exposed to this peril, there has been only a single event that was declared to be a natural disaster since the Nat Cat scheme began in 1982, namely, the April 2007 eruption on Réunion. That eruption had only marginal cost for the insurance industry, because the lava flows affected very little insured property. There was no official assessment of the total economic cost, but it was at all events minimal, even though a main highway was cut off for two months and entry into tourism and fisheries areas was prohibited while the lava flowed into the ocean.

The plethora of natural hazards connected to volcanic eruptions means that there is a not inconsiderable likelihood that French territory will be affected by an event similar to or even more destructive than the eruption of the Cumbre Vieja Volcano in the Canary Islands.

Exposure in the territory of France

Most volcanic activity is related to plate tectonics. As a general rule active volcanoes are concentrated along the edges of those plates, especially in subduction zones like Guadeloupe and Martinique. Volcanism in those places is ordinarily explosive, with pyroclastic flows and ash plumes. Volcanic activity is episodic, with dormant periods that can last for centuries. This makes it difficult for the insurance industry to estimate this risk.

Other types of volcanic activity are caused by "hot spots" located far from the edges of the plates, locations that are permanently fed by a magma source, such as Réunion in France or the Canary Islands in Spain. Volcanism in these locations is effusive, with lava fountains and flows. Eruptions may occur often (on Réunion, 173 eruptions in 350 years), but their impact tends to be limited.

Metropolitan France is close to a hundred extinct volcanoes, particularly in the region from the Massif Central to Catalonia in Spain. Though now extinct, the volcanoes in the chain of Puys in Auvergne were active until just 7,000 years ago.

The hazards of volcanic eruptions

Volcanic eruptions have a range of repercussions, and having in mind the different volcanic contexts in metropolitan and overseas France, could give rise to declarations of a series of natural disasters.

Lava flows

Lava flows (Figure 3) run down the flanks of volcanoes from craters or fissure vents, as is the current case on the island of La Palma. On the scale of volcanic risks, the danger to the population is low, because there is usually time to escape, although the potential for destruction is high due to buried infrastructure and the devastation caused by the advancing lava, not to mention the fires that are produced.

Figure 3. Lava fountain (roughly 200 m high) and lava flow from the Pu'u 'O'o Volcano in Hawaii in 1984.

Source: USGS.

Collapses and landslides

Collapses (Figure 4) are associated with the formation of a caldera from the collapse of a volcano's magma chamber. Collapses of the flanks are generally related to magma pushing into the volcano's structure, with progressive transformation of the rock, or to a landslide caused by a large earthquake. The impact of this phenomenon depends on its speed and on the volume of material displaced. The main dangers to infrastructure are destruction caused by burial and impact, changes to terrain, the formation of barriers in watercourses which can give rise to major flooding when they give way, and the generation of tsunamis.

Figure 4. Collapse of part of Mount St. Helens (USA) after the 1980 eruption.

Source: USGS.

Pyroclastic flows

Pyroclastic flows (Figure 5) are pieces of lava and rocks moving at very high speed (up to 700 km/h) in a cloud of extremely hot gas (from 200 °C to 1,000 °C). They are often formed when an overly dense ash plume collapses in on itself or when a lava dome collapses. Without a doubt it is the most destructive volcanic hazard: entire cities can be razed in minutes, as happened to Pompeii in the year 79 CE.

Figure 5. Ash column destabilisation and start of pyroclastic flow at Mount St. Helens (USA) in 1980.

Source: USGS.

Volcanic gases

Water vapour is the main volcanic gas, along with numerous acidic and sometimes lethal gases that increase the production of acid rain, which damages buildings, crops, pasture, and drinking water supplies. In 1986 a pocket of some 1 km3 of CO2 that had collected at the bottom of Lake Nyos (Cameroon) suddenly erupted and in a very short time killed more than 2,000 people.

Lahars

Lahars are flows consisting of mud, ash, rocky debris, and other materials mixed with water from a lake in the crater, rivers, sudden snow or ice melts, or simply rainwater. Slides of unconsolidated volcanic deposits can occur a number of years after the deposits were laid down. These slides can be devastating, for example the case of Armero (Colombia) located 45 km from the Nevado del Ruiz Volcano, where some 23,000 people lost their lives in 1985.

Ash plumes

Explosive eruptions can eject ash plumes up to more than 40 km into the air (Figure 6). Ashes are small bits of lava and/or rocks, variable in size and shape, that tend to be extremely abrasive. Breathing in the ash can cause respiratory difficulties. Major infrastructure risks include roof cave-ins from the build-up of sometimes wet ash. Mechanical systems that suck the ashes in can also be affected, for instance, land vehicles and aircraft. A good example of this was the 2010 Eyjafjallajökull volcanic eruption in Iceland, which forced 28 European countries to close all or part of their airspace and caused economic losses that the European Commission estimated at between 1,500 and 2,500 million euros.

Figure 6. Ash plume from the Mount Pinatubo (Philippines) eruption in June 1991.

Source: USGS.

Other hazards: earthquakes, tsunamis, and explosions

Earthquakes caused by volcanic activity are usually limited to active zones and tend to be low in magnitude (M<4). A recent case that affected France is recounted below and changed our perception of this hazard associated with volcanic activity.

Volcanic tsunamis are generally caused by large lahars, pyroclastic flows, or flank collapses that slide into the ocean. Local tsunamis of this kind are harder to monitor and control than tsunamis triggered by strong earthquakes.

Lastly, we should also mention the explosive propagation of shock waves following a volcanic eruption. They pose a major hazard to infrastructures, buildings, and people. These blasts are similar to those caused by industrial accidents or terrorist attacks, but because of the size of volcanoes, they can cause damage over hundreds of kilometres. For example, after the Mount Tambora eruption in Indonesia in 1815 damage was reported up to 400 kilometres away.

One event that France remembers is the eruption of Mount Pelée in Martinique in 1902

On the morning of 8 May 1902, 29,000 people lost their lives in just a few minutes when a pyroclastic flow from Mount Pelée completely destroyed the city of Saint-Pierre, then the capital of the Department of Martinique (Figure 7).

The cloud of burning material engulfed Saint-Pierre at an estimated speed of 180 km/h and a temperature of around 300 °C. It was preceded by a shock wave travelling at nearly 450 km/h.

In addition to the thousands of victims, the socioeconomic repercussions of this eruption were extremely important: thousands of people lost their homes and were forced to leave their lands, which were made unreachable and uncultivable for decades. Saint-Pierre, the capital of the Department of Martinique and the economic centre of the French Antilles, had to be abandoned, and the capital was moved to Fort-de-France, located outside the volcano's direct hazardous area.

Figure 7. Mount Pelée (Martinique) after the 1902 eruption. Pyroclastic flows reached the sea and the city of Saint-Pierre in a matter of minutes.

What impact would an event like the 1902 eruption in the Antilles have today?

Precise economic estimates for an event of this kind are hard to make, because the physical scars of the eruption and its socioeconomic effects would be felt at a regional scale for many years. The total economic cost might be put at more than 10,000 million euros.

Fortunately, the return period for events like these involving volcanoes of this kind tend to be several centuries. At any rate, Mount Pelée has since 2020 shown signs of new volcanic activity unlike those observed in previous decades. A major eruption could today be predicted weeks or months in advance based on the record of eruptions by this volcano, quite unlike that of Cumbre Vieja in the Canary Islands.

The question could be addressed before the eruption, and the costs relating, for instance, to evacuation of the population could be defrayed by a body to be decided, inasmuch as the natural catastrophe compensation scheme in France is designed only to cover material losses that have already occurred.

This situation may seem implausible, but it already occurred in Guadeloupe in 1976, when there was a recurrence of some activity that ultimately caused very little damage despite a score of blasts and numerous landslides. At the height of the eruption, an evacuation of the surrounding population in July 1976, at first spontaneously by around 25,000 people, subsequently followed by another of around 75,000 people over nearly half the island ordered by the authorities lasted for around five months.

Mayotte: the birth of a new submarine volcano

The island of Mayotte, French territory in the Indian Ocean, is a part of the active volcanic archipelago of the Comoros. The last volcanic activity on Mayotte proper is estimated to have occurred around 500,000 years ago.

Mayotte has been undergoing intense seismic activity since May 2018, with more than 1,500 tremors with a magnitude greater than 3.5 felt by the population. A distinctly stronger earthquake, magnitude 5.8, took place on 15 May 2018 and caused considerable damage on the island. The combined seismic activity that has occurred since 2018 was declared a natural disaster, which brought entitlement to compensation as stipulated under the insurance scheme.

In parallel to this unusual seismic activity, high-precision GPS devices located on the island have recorded displacement of the island about 25 cm to the east together with drop in elevation of 10 to 20 cm.

All this seismic activity and movement of the island as a whole is related to the emergence of a volcano on the ocean floor some 50 km east of Mayotte. Scientifically speaking, this is an extremely rare and exceptional event that has been able to be documented for the first time thanks to modern methods of observation. At this time the submarine volcano has grown to a height of over 800 m above the sea bed, and continued growth over the coming years, decades, or centuries will give rise to sporadic incidents and occasional damage on Mayotte.

While infrequent, volcanic eruptions and their repercussions on the population, buildings, infrastructure, and socioeconomic fabric of the affected territories can represent major events for different insurance industry lines all at once, e.g., personal injury, property damage, motor vehicle, marine, and aviation insurance, etc., like few other natural catastrophes can produce.

Up to now there have been few large-scale eruptions in territories with mature insurance markets accustomed to handling losses of several thousand million euros a year caused by hurricanes or earthquakes around the world. The Cumbre Vieja eruption in the Canary Islands is a recent example, and historical eruptions in the territories of France should remind us that this peril exists and that it needs to be quantified and included in assessments of our exposure, so that we can ensure continued operation of special compensation schemes for natural catastrophes like the CCR, which plays a central role in France, or the Consorcio de Compensación de Seguros in Spain.

Despite the fact that French territory, its overseas territories in particular, are exposed to this peril, there has been only a single event that was declared to be a natural disaster since the Nat Cat scheme began in 1982, namely, the April 2007 eruption on Réunion. That eruption had only marginal cost for the insurance industry, because the lava flows affected very little insured property. There was no official assessment of the total economic cost, but it was at all events minimal, even though a main highway was cut off for two months and entry into tourism and fisheries areas was prohibited while the lava flowed into the ocean.

The plethora of natural hazards connected to volcanic eruptions means that there is a not inconsiderable likelihood that French territory will be affected by an event similar to or even more destructive than the eruption of the Cumbre Vieja Volcano in the Canary Islands.