1. Introduction

Following a brief reference to the range of protective instruments, this article will centre on one of them, singularly Spanish and of very special relevance. The instrument concerned is the legal system for the assessment of the personal injury damages caused to people in traffic accidents, which has undergone a very recent process of review and in-depth reform.

In the following pages the intention is not to provide an exhaustive description or an analysis of the final system resulting from the review, in force as from 1 January 2016. By the time these few lines have been published, many articles, studies, training sessions and events of all kinds and from different points of view will have been dedicated to this purpose and no doubt will continue to appear in the future.

The objective -much more limited- which is sought here is to offer a few key elements which, taken overall, could perhaps facilitate the reader's understanding of the extraordinary usefulness of this protective instrument, of its enriching evolution, of the orientation given to its recent reform and of the risks involved, not only due to the absence of such an instrument but also from a restrictive or abusive or, in the end, an unbalanced application of it.

2. The legal mechanisms for the protection of traffic accident victims

The protection of traffic accident victims is achieved through a set of legal instruments which facilitate a fair, certain and rapid compensation for the damages caused by the drivers of motor vehicles responsible for accidents. To sum up, the principal measures of protection in the scope of the European Economic Area are as follows:

- The legal obligation of insuring liability in motor vehicle traffic. In Spain this legal obligation falls upon the owners of the vehicles.

- The establishment of a Guarantee Fund for the compensation of victims in those cases where the compulsory automobile insurance mechanism is unable to act. This occurs in cases where an accident is caused by a vehicle operating without having complied with the legal obligation of taking out insurance or where it has not been possible to identify the vehicle responsible. In the case of Spain the Guarantee Fund functions are attributed by Law to the Consorcio de Compensación de Seguros (hereinafter, the CCS), a public entity belonging to the Ministry of Economy and Competitiveness. In addition to the two situations mentioned above, the CCS also has been assigned two additional functions in the framework of its Guarantee Fund status: the payment of compensation to victims of accidents caused by stolen vehicles and vehicles whose use was unauthorised, and to the victims of accidents caused by vehicles which, although insured, were covered by an insolvent insurance undertaking already dissolved or in the process of being wound up.

- The taking of direct action by victims against the insurance undertaking of the vehicle responsible for the damages caused in an accident, thereby avoiding the need for the victim to have to file a claim against the driver of the vehicle. In our country, the institution taking direct action against the insurance undertaking was already legally provided for prior to the requirement established in the Community directives.

- The establishment of an informative mechanism that would enable accident victims to quickly ascertain the identity of the insurance undertaking of the vehicle responsible for an accident in order to lodge a claim. In Spain, the legislation on motor vehicle civil liability and insurance created the Insured Vehicle Information Database (Fichero Informativo de Vehículos Asegurados - FIVA) and entrusted its management to the CCS.

These four protective mechanisms–the compulsory insurance; the Guarantee Fund; the direct action against the insurance undertaking or against the Guarantee Fund, as appropriate in each case; and the system for identifying the insurance undertaking when lodging a claim for compensation- have been complemented in Spain by two other instruments specifically designed for cases requiring additional protection, that is, accidents involving personal injury. These are two instruments which do not stem from the European Union Directives on automobile civil liability and constitute an extremely important asset in Spanish automobile insurance, enriching it in comparison to the insurance requirements in other countries in our region, and facilitating the hospital care of victims and the payment of compensation for personal injury damages. The two mechanisms unique to our country, which are referred to here, are as follows:

- The signature of agreements –for which legal provision has been made- between the hospitals and the emergency services that care for accident victims, on the one hand, and the insurance undertakings and the CCS who pay compensation to the victims, on the other. These agreements, which are renewed on a regular basis, are entered into both with the public and the private hospital networks. The agreements establish clear, automatic rules for determining which insurance entity is under the obligation of paying for the care provided without the need for waiting until the civil liability emanating from the accident giving rise to the care has been determined. Moreover, these agreements regulate the requirements, time limits, procedures and prices to be invoiced, together with mechanisms for settling discrepancies. All of this, without a doubt, leads to a more harmonious and stable operation of the insurance and of the medical care system, to the benefit of the hospitals and insurance undertakings alike, as well as, in the end, of the injured parties who require medical care. However, the advantages go even further, since these agreements, as a consequence of the foregoing, have the essential virtue of circumscribing the economic relations to the hospitals and the insurance undertakings (or to the CCS as the Guarantee Fund), in such a way that the accident victim cared for by the emergency service and by the hospital is therefore exempt from having to advance the payment for the care received.

To sum up, through these agreements, accident victims and their families are relieved from the uncertainties and concerns they would have to face in the absence of an agreement, in terms of not knowing who is finally liable for meeting the costs of the medical care they are receiving and whether they can be asked to advance the amount of the costs involved.

- The application of a legal scheme for assessing the personal injury damages in traffic accidents. This scheme is commonly known as the “Scale” (Scale), a term which is still inexact because it does not reflect the full scope of the compensation mechanism it encompasses, but which will be used here for reasons of brevity and convenience. The Scale, as it stands at the present time, was created through additional provision eight of Act 30/1995, of 8 November, its most recent precedent in time being an Order issued by the former Ministry of Economy and Finance dated 5 March 1991. We are thus looking at a unique protective institution, pertaining to the Spanish insurance scheme, which is an essential part of the history of automobile insurance in our country during the last twenty-five years. The rest of the content of this article will be devoted to an explanation of the reasons for the existence of the Scale and of its very recent update through a process of in-depth reform.

3. The necessary precedent: the indicative Scale of 1991

The origin of the Spanish Scale –not the most remote scale but the one closest to our present-day reality and concerns- goes back to the end of the eighties and the early nineties of the past century, that is, almost thirty years ago.

We found ourselves at that time in a complex and confusing context, in which the judicial proceedings dealing with traffic accidents were characterised by extremely variable petitions by prosecutors and court decisions, depending on the territory where the proceedings took place, and with a clear trend towards higher economic settlements without apparent control or sufficient argumentation. This context, in turn, encouraged lawyers representing injured parties to seek increasingly higher compensation payments. The lack of guidelines for the quantification –not even approximate- of compensation made it difficult to reach agreements between insurance undertakings and injured parties, drawing out the discussions and either giving rise to litigation or preventing dejudicialisation, according to each case. That panorama of instability made it extremely difficult for insurance undertakings to calculate insurance premiums on a technical basis and the technical provisions to be put into place. Also, the supervisory authority indicated its concern over the unquestionable repercussions of this situation on the solvency of the insurance undertakings and the fact that the non-existence of rules for establishing compensation prevented the calculation, with the necessary certainty, of the level of sufficiency or insufficiency of the rates applied by the insurance undertakings and of the technical provisions accounted for by them.

It was in this context when the Order of the Ministry of Economy and Finance of 5 March 1991 was promulgated, as an outcome of an exemplary course of action coordinated between the supervisory authority (the then Directorate General for Insurance in the Ministry of Economy and Finance) and the most representative associations of the private insurance sector.

A closer look at two aspects of this episode is worthwhile, as, in our opinion, it constitutes a genuine milestone in the history of Spanish automobile insurance: the real value of this Ministerial Order and the strength of its Explanatory Statement.

The low rank and the merely indicative and in no way mandatory nature of the text approved neither reduced nor restricted the relevance of the legal provision published in the Spanish Government gazette, the

Boletín Oficial del Estado, on 11 March 1991. Both the insurance sector and the supervisory authority were fully aware of the limitations of the provision and, therefore, on supporting and approving it, they were not acting in a “naive” manner, as some sectors of opinion voiced at the time. The objective was to arrive at a mandatory Scale which, therefore, would have the rank of a law passed by Parliament. However, in order to succeed in attaining that objective, it was necessary to take a first step forward, to create an appropriate atmosphere that would make it possible to finally obtain a mandatory Scale. The Ministerial Order was the adequate first step in order to gradually generate an atmosphere among judges and prosecutors that would –some time later- enable the implementation of a compulsory Scale.

The second aspect refers to the content of the Order, in that the Explanatory Statement or preamble to the Ministerial Order of 5 March 1991, in our opinion, played a unique role by serving as a true “Manifesto” in favour of the Scale. In very clear, measured and orderly terms, it explained the reasons why having a Scale for establishing the compensation to be paid for personal injury damages constituted an unquestionable advantage for all concerned –victims, private insurance undertakings, judges and prosecutors-. The 1991 Explanatory Statement is fully applicable to 2015, as it is essential both for understanding the confusing initial situation which the Order sought to combat, as well as for understanding the advantages of the existence of a legal Scale and the risks that would no doubt arise in the event of the disappearance in the future of this instrument of compensation. A reading of this Statement by those who did not experience the pre-scale stage of our automobile insurance is a highly recommendable exercise. In view of the foregoing, I believe that it is appropriate and not at all superfluous to recall the six aspects highlighted repeatedly by the aforementioned preamble, constituting the reasons which, twenty-five years later, continue to render this instrument of compensation indispensable.

- Introduce a mechanism of certainty, thereby complying with the principle of legal certainty enshrined in article 9.3 of the Spanish Constitution.

- Further similar treatment for situations of liability in which the issues at stake coincide, through application of the principle of equality enshrined in article 14 of that fundamental text.

- Serve as a framework and stimulus to the use of compromise agreements, making them the priority procedure for the settlement of claims.

- Streamline to a maximum degree the payments for claims by insurance undertakings, avoiding delays detrimental to the beneficiaries, on not having to wait for the decision of judicial bodies.

- Reduce the legal actions in this sector significantly with a consequent decrease in the generalised heavy workload of the Courts.

- Finally, enable the insurance undertakings to make forecasts based on reliable criteria, with unquestionable transcendence for the solvency of these undertakings and the performance of their functions.

4. The mandatory Scale of 1995 and its shortcomings

Twenty years of practical application of the 1995 mandatory Scale is a long time in which significant structural insufficiencies could hardly fail to have been detected or critical voices could scarcely fail to be heard –some in acid, exaggerated and at times even demeaning terms- against it. To simplify and avoid excessive detail, it was said even from the very start that the Scale was extremely simple –leaving out many situations deserving of compensation- and the amounts included were far too low. Applying 2015 standards, both criticisms are true; however, they need to be looked at from the perspective of time.

It appears now very normal to have a mandatory Scale when we have had it for the last twenty years. However, we should not lose sight of the fact that it was necessary to overcome much reluctance in order to obtain its approval. To begin, the authorised voices in the eighties and nineties who considered that a mandatory Scale would constitute an intolerable attack against the principle of judicial independence were not few in number. At the same time, many of those who accepted the idea of a mandatory Scale in principle insisted that this novel instrument should be easy to interpret and easy to apply in practice. To sum up, the atmosphere at the time was more favourable towards proposing a simple instrument, without too many ins and outs and with a speedy administrative procedure.

The lack of experience with earlier Scales, the need for acting quickly in the processing of the proposal and the advisability of putting forward an instrument that could be perceived in the judicial environment as easy to apply in daily practice are circumstances which led to the situation where the 1995 Scale was finally given a structure that was perhaps excessively schematic or simplistic. Had there been a more complex approach with more extended discussion at the time, we would not have had a mandatory Scale in 1995. The greatest obstacle at that time –or at least it was perceived as such- was to try to demonstrate that a Scale of a mandatory nature would not have to be necessarily contrary to the respect for judicial independence, and this is the reason why it was decided to establish sufficiently broad brackets between the maximum and minimum amounts to be paid in respect of some of the losses eligible for compensation. There was even criticism in the sense that the broad scope of some of the compensation brackets would make it difficult to achieve friendly out-of-court settlements and would be an obstacle in practice for giving similar treatment to coincidental situations, as required by the principle of equal treatment enshrined in article 14 of the Spanish Constitution.

Moreover, there were discussions with respect to the insufficiency, in general, of the amounts of compensation included on the 1995 Scale. With the passage of time this criticism, logically, has grown stronger. There is no objection to the need to update the amounts stipulated on the Scale, however, it is also necessary to take into account that the situation of the insurance sector between 1990 and 1995 was not as sound as it is today and that the reality of society was very different from that of 2015. The Administration responsible for leading the legislative proposal clearly saw –as could not be otherwise- that the new mandatory Scale had to be, at the same time, a markedly protective mechanism, an instrument of legislative politics that would contribute stability to the insurance undertakings supporting the system. The idea that it was necessary to obtain rapid out-of-court settlements without endangering the level of solvency of the insurance sector was unanimous.

Having said this, no one doubts the insufficiencies of the 1995 Scale from our current perspective. Setting aside polemical issues, there is agreement on -

inter alia- the following relevant aspects:

- In the 1995 Scale, the principle of legal certainty prevailed over the principle of compensatory justice. The Scale was a magnificent instrument for standardising compensation and for determining the amounts to be paid with certainty and speed, but left some situations of unquestionable relevance without adequate compensation, such as the loss of earnings.

- Moreover, a separation between moral or extra-patrimonial damages and material damages is missing and, within these, between the concepts referring to general losses and the loss of earnings.

- With respect to the material damages, the Scale, on multiplying the percentage of the net earnings from the personal work of the deceased or injured victim by the amount of the compensation for moral damages, makes a complete abstraction of the future expenses the injured party may have to incur or the future income which the family of the victim could reasonably be presumed to lose in the case of death, or the injured party him or herself. In the case of moral damages, which measure the intensity and the duration of the pain and suffering due to death or injury, it appears fair to compensate this by means of the application of conventional amounts; however, the full compensation of the material damages calls for specific calculations more closely adjusted to the reality of the expenses incurred and of the income not received, without prejudice to having to recur to explicit and reasonable hypotheses.

- Similarly, insufficiencies in the compensation of disabling injuries (i.e. the need for assistance by a third person to care for the injured party) have been evidenced, as well as the non-existence of some concepts due for compensation, such as home care.

On the basis of the preceding clearly identified insufficiencies, case law has also opened a few cracks in the Scale, as decisions have been handed down which have increasingly departed from the compensations determined on it.

Finally, to prevent the progressive deterioration of the system and a return to the situation of generalised confusion that gave rise to the Ministerial Order of 1991, it was necessary to address the reform and updating of the 1995 Scale.

5. The process for the reform of the Scale

A number of the specialities of the reform process carried out between the end of 2010 and June 2014 deserve mention, as this will help to achieve an understanding of the Scale finally approved.

In the first place, the process for the revision of the 1995 Scale and for the drawing-up of the proposed new Scale was carried out with the active and ongoing participation of all of the sectors involved. The Ministries of Economy and Competitiveness and of Justice appointed a Committee of Experts (hereinafter, the CEX) which included representatives from associations of traffic accident victims and insurance undertakings, that is, those who should receive compensation and those who must make compensation payments. In addition, the CEX also included representatives from the Office of the Public Prosecutor for Road Safety, the Ministry of Justice, the CCS, solicitors specialised in automobile civil liability insurance law and from the Institute of Spanish Actuaries.

The second unique feature consisted of the focus and the scope of the work for the review and preparation of the proposal by the CEX. In contrast to the more usual option consisting of the submission of a report by the group of experts identifying the deficiencies of the current legal provision and setting out the principles and standards on which the reform should be based, indicating the diversity of opinions and of alternatives, if any, on this occasion the CEX chose to present a specific and complete proposal for a new Scale. The CEX submitted a full text of articles and compensation tables, also complete in their structure and amounts.

The third unique feature of the entire process of review undertaken –and which in the end was the most decisive for the success of the process- consisted of the fact that the full proposal of the text of articles and compensation tables was submitted after having achieved a consensus among the members of the CEX. Undoubtedly, in the course of the many working sessions of the CEX, very diverse criteria and opinions were voiced in which, as can be expected in a forum where conflicting interests were represented, discrepancies were frequent. However, rather that the initial idea of submitting a proposed text of articles that would include, in addition to the wording agreed by the majority, the various individual votes and dissenting opinions on all of the issues on which significant differences would have arisen, an idea was gradually developed in the direction of focussing the Committee’s effort on the attainment of a final proposal agreed by consensus for the purpose of facilitating the administrative procedure, in the first place, and then the subsequent parliamentary process for the legal provision proposed. With this orientation, the members of the CEX strove to limit their individual votes or observations to a minimum considered indispensable, that is, to issues truly transcendental. However, in the final stretch of sessions of the CEX, the idea wisely prevailed determining that, in the process of reducing discrepancies, it was worth making an additional effort to achieve a complete consensus. In May 2014, during the final sessions held at the University of Girona, a full agreement was reached that included the text of articles, the structure of the entire series of compensation tables to accompany the text and the economic amounts and quantitative limits to be included, depending on each case, in the text of articles or the tables. Following this final consensus –a result of significant and certainly meritorious effort, which went on to be known in the environment of the CEX as the “Girona Pact”-, the CEX submitted the full proposal for the new Scale in June 2014.

The full consensus reached, and most especially the fact that the consensus included –as was explicitly documented in writing- the agreement between the representatives of the traffic accident victims and of the insurance undertakings, turned out to be the determining factor for the quick and successful processing of the proposal, both in the administrative channel as well as in Parliament.

In fourth and last place, and a logical consequence of the second and third unique features noted previously, the review and reform process carried out was very lengthy. First, on account of the scope of the work performed, since, from a simple Scale with many automatisms as was the case of the 1995 Scale, the intention was to move on to a more complex Scale, based on the principle of full reparation for the victim, with many more compensation concepts and shades of meaning. Second, because this greater complexity and extension inevitably meant that many subjects of debate would arise. And, finally, as already mentioned, because the intention was –and was successful- not to leave any of these discussions open and always to reach an agreement among the different opinions. The process commenced in 2010 and concluded in June 2014, which gives an idea of the difficulties of the task performed. However, contrary to the idea that there was excessive delay in the preparation of the proposal, the idea should prevail that, in compensation for the delay, the CEX submitted a full, sound and agreed proposal, in such a way that many of the debates that surely would have arisen during the processing of the draft legislation, leading to a costly, polemic and drawn-out process, were taken on by the CEX itself. To sum up, much time was used in the preparation of the proposal, but very little time was necessary for the administrative and parliamentary processes of the preliminary draft and the bill, respectively.

6. The guiding principles of the reform and the balance of the assessment system

The principles guiding the new Scale, which has finally been approved, are those contained in the Order issued by the Ministries of Economy and Finance and of Justice on 12 June 2011, officially establishing the CEX, which had already been operating under another format since 2010. In accordance with the content of that Order, the proposal for the reform of the Scale had to:

- respect the principle of the integrity of the reparation of the damage, in order to restore the victim to a situation as similar as possible to the situation the victim would have had, had the accident not occurred;

- observe the structuring principle, consisting of the need to clearly separate the assessment of the extra-patrimonial or moral damages from those of a material nature, in their dual facet as general losses and loss of earnings;

- facilitate a certain and quick quantification of the compensation and a rapid achievement of agreements between the injured party and the insurance undertaking of the party responsible for the accident.

That is, the new Scale must be understood as a set of elements that seeks to maintain a balance –certainly very necessary but very complicated to reach- between opposing factors.

On the one hand, the principle of full reparation, which is basic, calls for identifying types of injured parties and damages to be repaired which are not included on the 1995 Scale; to systematise and give the regulation of the compensation for loss of earnings, considered in the 1995 Scale in a significantly simplistic and insufficient manner, a substance of its own; and to raise the amount of the compensation in many cases, as occurs in cases of disabling injuries or in those of minor children of deceased victims.

However, the fact is that this greater wealth of types of damages and of situations to be remedied and the greater complexity of the calculations to be made could become an obstacle for the attainment of another of the guiding principles which, in our opinion, is essential to preserve in order for the compensation system to be operative and agile in day-to-day practice, which is that of developing an instrument for quickly arriving at friendly agreements between the injured parties and the insurance undertakings or the CCS. Thus, express provision was made for this, as already mentioned, in the Order creating the CEX, and we should not forget how the Ministerial Order of 5 March 1991, in the preamble already discussed, not only conceived the Scale as an adequate instrument for encouraging compromise agreements, but also sought to make them a “

priority means for the settlement of claims”. One of the greatest challenges in the immediate future will be to apply the new Scale judiciously –“to apply” it not only when offering an amount as compensation, but also when submitting a claim for compensation and on justifying the damages claimed-, in such a way as to ensure that the new possibilities which the new framework wisely and fairly offers do not bring with them a return to the litigation culture.

At the same time, legal principle of full reparation which inspires the new Scale and which, as has already been highlighted, includes a significant increase in types of damages and amounts of compensation, must be in consonance with the principle of economic sustainability of the system overall. This sustainability resides in the existence of compulsory insurance and, consequently, the payment of insurance premiums which are affordable for motor vehicles owners and compensation payments which can be assumed by the insurance undertakings. The economic sustainability of the system also calls for a level of a reasonably supportable intervention by the Guarantee Fund –the CCS-: the level of the amounts of the insurance premiums should not lead to a significant increase in the number of uninsured vehicles, while the increase in the amount of the compensation payments should not give rise to applications for bankruptcy among insurers. That is, the principle of full reparation must be in consonance with the social reality and must not place compliance with the obligation to insure or the technical and solvent operation of the insurance sector at risk.

It is on account of the foregoing why, in a global vision of the new Scale, together with new injured parties to be paid compensation, new types of damages to be repaired and higher amounts, some restrictions can be observed which not only have a moderating effect on the economic impact of the new Scale, but also confer automatisms and certainties which are essential, in our opinion, in order for the practical application of the Scale to take place in most cases speedily and through agreements instead of going down the road of discrepancy and judicial litigiousness.

It is in this terrain where the configuration of the damage assessment system acquires particular relevance as a “closed” and “comprehensive” Scale. This is indispensable, in our opinion, for eliminating uncertainties in the quantification of compensation, in order to further friendly agreements and put obstacles in the way of the litigating spirits, and to facilitate speed in the processing and payment of the claims by insurance undertakings and the CCS. The new Scale dispels these fears through the “objectification of the damage”, by virtue of which compensation cannot be established for damages or amounts other than those included on the Scale. However, together with that express recognition of the claims-rated and closed nature of the Scale, the Scale -on the basis of the principle of full reparation- also expressly provides for the possibility that damages to be compensated could exist which, despite the detailed regulation, would not have been included on the Scale, although treating them in line with the exhaustive nature of the Scale in order to maintain the difficult balances we referred to previously.

And in this way, the new Scale, as we understand it, refers -in considered and balanced terms- to “significant” losses caused by “unique” circumstances which would not have been taken into account, due to such uniqueness, in the rules and limits of the Scale. It describes them as “exceptional losses” for which compensation is paid within the system itself, and establishes a ceiling –also weighted- of 25% of the basic compensation.

7. The structure of the new Scale

In comparison to the 1995 Scale, the new Scale has a much more extensive structure, but also much clearer, and this is a consequence of its having been built on the combined foundation of the principle of the full reparation of damages and the principle of the structuring of the different components of the damage. In the context of the first principle mentioned, the aim was to ensure that no significant damage would fail to be assessed, in such a way that the victim would finally be in a situation as close as possible to that which the victim would have had, had the traffic accident generating the damage not occurred. This signifies that the new Scale adds many elements which were not included on the 1995 Scale and, consequently, that it is richer, has more shades of meaning and greater complexity, and is much more extensive than its predecessor. However, at the same time, the structuring principle contributes clarity: an effort has been made to clearly separate the moral or extra-patrimonial damages from the material damages; that, in turn, the same clarity exists in the separation, in the context of the latter damages, between general losses and the loss of earnings; and that, finally, on identifying and delimiting the types of damages eligible for compensation within each of these categories and the relevant amounts, no damages are left without compensation and no types of damage or amounts of compensation are duplicated.

Despite the extension and complexity of the new Scale, the compensation structure is clear and simple. The Scale is divided into compensation for death, compensation for sequelae or permanent injuries and compensation of temporary injuries, and in each of these categories, a distinction, in turn, is made between three types of damages:

- The basic personal damages: moral damage common to all victims or injured parties of a certain category.

- The specific personal damages: damages eligible for compensation and the relevant amounts of compensation to be paid for individualised moral damages for each victim or injured party in view of their specific circumstances of a personal, family, economic or social nature.

- The material damages, in which, in turn, a distinction is made between the types and amounts for general losses (expenses incurred as a consequence of the accident) and loss of earnings (loss or reduction of income or of the capacity to obtain earnings).

The structure of the text in articles is taken likewise to the tables, which set out the amounts to be paid as compensation. There are series 1 tables for death; series 2 reserved for sequelae or permanent injuries and series 3 for temporary injuries. Each of these three series of tables is made up, in turn, by A tables, for basic personal damages; B tables, for specific personal damages plus the exceptional damages and C tables, which refer to the material damages (in the two categories, as mentioned earlier, of general losses and loss of earnings).

8. Significant new developments in the 2015 Scale with respect to 1995

The purpose of these few lines is not to analyse the content of the aforementioned structure in detail, however, without intending to take an exhaustive look at the structure, we are setting out below a number of significant new developments in each of the preceding categories.

8.1. Compensation for death

The compensation structure is completely new, to the extent that it is advisable to avoid automatic and simplistic comparisons between the amounts of the 1995 Scale and those of the new Scale. And, in contrast to what has been occurring up to now, where a higher or lower amount of compensation depended on the family structure of the victim, the new Scale is comprised by five autonomous categories of injured parties (the widowed spouse, the ascendant relatives, the descendant relatives, the brothers and sisters and the close associates), each of whom receives a basic amount, regardless of whether there are other injured parties or not and regardless of whether these parties are in the same or in other categories. The new system stems from the idea -a wise notion in our opinion- that the existence of moral or extra-patrimonial pain and suffering and their intensity does not depend on the existence of other injured parties. Some relevant circumstances of the family environment may certainly be a subject for consideration and assessment, such as situations of loneliness of the injured party, however, on the basis of the earlier-mentioned structuring principle, these circumstances should be assessed in a radically separate manner, within the scope of the specific damages –and not in the basic- of the recipients of the compensation.

Secondly, the new Scale takes into consideration new injured parties not included on the 1995 Scale. This is the case of the “close associates”, who, with prudent criteria, are restricted by certain requirements of affection and living-together with the victim and with the establishment of a limited amount of compensation, as well as in the case of the brothers and sisters of the victim. The latter, in the 1995 regulation, received an insignificant amount of compensation, or even received none, depending on the family group in which they were included on the Scale –a division no longer found on the new Scale.

Thirdly, the new systematic and exhaustive regulation of the specific personal losses stands out, that is, the compensation additional to the basic fixed amount. Some situations that generate these supplementary compensation payments and which were not considered in the 1995 text include the physical or mental disability of the injured party as a result of the accident (and not only prior to its onset); the living of the injured party together with the victim; the situations of significant solitude of the injured party, that is, situations where the injured party does not share the pain and suffering with another injured party of his or her same category or where the injured party is the sole relative of the victim; or in the case of the death in the accident of the sole parent of the injured party.

Finally, the detailed regulation of the material losses occasioned by the death of the accident victim are of great significance, together with the fact that this regulation has been approached from the perspective of the aforementioned structuring principle, completely separate from the damages of a moral nature (basic personal damages and specific personal damages). All of this in contrast to the simplistic 1995 solution, in which the economic damages were limited to a percentage applied to the basic damages, differing in line with the level of income of the victim. The new regulation makes a distinction between damages eligible for compensation as general losses (reasonable expenses derived from the death, with the payment of the amount of 400€ without having to justify expenses or a higher amount if documentary proof is given) and as loss of earnings. In this latter case, the fact that the loss of earnings is eligible for compensation solely if there is an economic dependency on the income of the victim stands out on the one hand, and on the other, the fact that the case of the dedication of the victim to home duties is taken into account as a form of contribution to the maintenance of the family unit. In this way, compensation is considered for exclusive dedication to the tasks of the household as well as for the partial dedication to such tasks (reduction of working hours for rendering remunerated employment compatible with the aforementioned household tasks).

8.2. Compensation for sequelae or permanent injuries

In the first place, the 1995 “medical scale” has been revised and improved, as the outcome of an analysis by consensus between a medical committee of the insurance undertakings and of the associations of victims, with the additional intervention of a CCS expert medical team for reaching a final decision on those sequelae for which no agreement had been achieved for their identification and assessment between the medical experts of the insurance undertakings and the associations of victims. The coherence of the economic assessment of the sequelae has also been improved, since the new Scale generates a different amount of compensation for each year of age of the injured party and for each point of assessment of the sequelae, instead of maintaining the doubtful configuration of the 1995 table by points and age brackets.

Secondly, and in relation to the specific personal damages, the regulation by the new Scale of the moral damages stemming from the loss of quality of life caused by the sequelae is significant. These damages encompass three differentiated aspects: the loss of personal autonomy, preventing or restricting the performance of the essential ordinary daily activities (eating, drinking, getting dressed, personal hygiene…); the loss of personal development, both in its individual as well as its social significance, preventing or restricting the performance of activities relating, for example, to enjoyment or pleasure, to a life of relationships, sexuality, leisure time or education; and that of holding a job or practicing a profession, not in their consideration as a means for obtaining economic remuneration –which, by virtue of the structuring principle is to be considered under the heading of material damages– but rather as an instrument of personal development which impacts decisively on the self-esteem of the injured party. The new Scale makes a distinction between very serious, serious, moderate and slight damages.

A new development in this same scope of the specific personal damages derived from sequelae is the regulation of damages due to the loss of quality of life not with respect to the injured party himself or herself but rather the members of the family of seriously disabled victims, in cases of the very serious loss of personal autonomy by the injured party requiring the assistance of the members of the family, substantially altering their lives.

A third development is particularly innovative, complete and systematised and consists of the regulation of the material loss caused by the sequelae. In terms of the general losses, there is a separate regulation of the foreseeable expenses of future health care of a lifelong nature in the scope of hospital and outpatient care; the expenses arising from the need for prostheses and orthoses; the expenses of rehabilitation in the home and in outpatient clinics; the expenses due to a very serious or serious loss of personal autonomy (technical aids, alterations to the home and the costs of mobility, this latter concept being broader than that of “adaptation of vehicle” applicable up to now); and the expenses of assistance by another person owing to a very serious or serious loss of personal autonomy.

In turn, with respect to the loss of earnings, the new Scale makes a distinction between the damage sustained by an injured party due to the partial or total loss of income from employment; that suffered by a person who is devoted totally or partially to the tasks of the family household; and that of persons who have not yet entered the labour market at the time when the accident occurred (basically minors or students who, due to the consequences, will not be able to hold a job or exercise a profession that will provide them income or who will find their options for holding a job and obtaining income seriously impaired).

8.3. Compensation for temporary injuries

In the first place, the consistency with which these compensations are addressed stands out. In coherence with the regulation of the compensation for death and permanent injuries or sequelae, the new Scale maintains the same scheme in the case of temporary injuries. As in the previous cases, a clear distinction is made between the amounts of compensation for basic personal damages, the amounts of compensation for specific personal damages and the amounts of compensation for material losses, with the distinction in the latter case -also mentioned previously- between compensation for general losses and compensation for loss of earnings.

The basic personal damage is equivalent to what in the 1995 Scale was referred to as a “non-impeditive day” and consisted of the ordinary loss all injured parties suffer from the date of an accident until the time when the process of the curing of their injury finalises or when the stabilisation of the injury and its conversion into a sequel occurs. This loss is compensated by means of a daily amount (30 €) which is somewhat less than the amount applicable on the 1995 Scale (31.43 €). This reduction is consistent with the intention of reinforcing the compensation system in cases of death and significant injuries and with the simultaneous need for not placing the sustainability of the system itself at risk. The reduction is insignificant but has a very appreciable economic impact, as it makes it possible to free up resources in favour of other sections of the Scale which were seriously in need of an improvement.

The compensation for specific personal damages consists of daily amounts which, for reasons of clarity, is paid at the basic rate of 30€, in such a way that the days referring to temporary damages are either basic or specific. These amounts for specific personal damages will vary depending on whether the temporary loss of quality of life experienced by the injured party is very serious, serious or moderate, a qualification which, in line with the pattern set in this regard in the case of permanent injuries or sequelae, will depend on how the temporary injury affects the exercise of the essential day-to-day activities or the specific activities of personal development. The damage caused by surgery is added to the scheme described earlier as a specific personal loss, with different amounts according to the characteristics and complexity of the operation and the type of anaesthesia.

In terms of the compensation for material damages, in addition to the general losses (“expenses of medical care” and “sundry expenses eligible for compensations”), the new Scale –in the case of loss of earnings and the same as in the rest of cases- does not provide for automatic compensation but rather a reparation circumscribed to those cases in which the temporary injuries have given rise to effective losses of income from the personal work of the injured party or with respect to the possibility of continuing the exclusive performance of the household tasks of the family unit.

Secondly, special mention should be made of the regulation of minor spinal column injuries (commonly known as “cervical whiplash injuries”). These are injuries which are diagnosed on the basis of the mere statements by the injured party concerning the existence of pain and cannot be verified by means of supplementary medical tests. The increasing frequency with which compensation has been sought from insurance undertakings and the CCS itself, on questionable grounds, for this kind of injury over the last few years has made it advisable to use caution in addressing the regulation of these injuries.

The new Scale does not pretend to be the instrument for eradicating fraud in this area, as it is fully aware that it is not the appropriate vehicle for this purpose. What it does pursue –and we believe that with considerable success- is that a mere reading of the text of the provision regulating these minor injuries clearly conveys to the reader the concern felt by widespread sectors of the social, institutional and professional environment, as well as by the Spanish insurance system overall, and how that concern has been effectively taken up and assumed by our legislators. This is why the legal text attempts to contribute a number of criteria to assist in discerning between applications that are well-founded and those that are abusive or fraudulent. Observe in this context how the new Scale:

- devotes a specific article to this type of minor injuries in the text of articles contrary to the alternative option which would have consisted of considering that we are looking at a strictly technical and medical issue, in which case the Scale should have limited itself –mistakenly, in our opinion- to including these injuries as just another sequela on the medical tables of the Scale;

- attributes to these injuries, in general, the status of “temporary injuries”, in comparison to the 1995 regulation which treated them as “sequelae” or “permanent injuries”;

- establishes causality standards for determining in each case where there is or there is not a genuine temporary injury eligible for compensation (i.e.: that there is evidence that the symptoms appeared with reasonable immediacy and that medical care was sought also with reasonable immediacy; or where there is compatibility between the injury claimed and the mechanism of the accident).

9. The Consorcio de Compensación de Seguros (CCS) and the Scale

The experience the CCS has in the application of the Scale is of particular interest, since in the majority of the cases in which it intervenes in its capacity as the Guarantee Fund compensating victims, significant difficulties arise which, in principle, do not normally occur in the claims processed by the insurance undertakings. Such difficulties constitute true obstacles for reaching, in practice, compromise agreements.

In those cases of accidents caused by vehicles which, in principle, appear as uninsured, only on very few occasions is the CCS able to obtain the version of the presumably uninsured driver about the mechanics of the accident, and cases where there are reasonable doubts about whether the insurance was or was not in force on the exact date when the accident occurred are also not infrequent.

In the coverage of damages caused by stolen vehicles, the difficulty for determining the exact circumstances in which the theft of the vehicle occurred (the CCS pays compensation in cases of a stolen vehicle or the unauthorised use of a vehicle, not in cases of theft), or the doubts as to whether first-degree intent concurred in the accident (not eligible for compensation) or whether wilful negligence was involved (eligible for compensation), are factors which contribute to making it difficult to reach a quick decision about the liability to be borne by the CCS as a Guarantee Fund and, finally, about the amount to be paid as compensation, if any is to be paid.

The decisions to be adopted in cases where the claim for compensation submitted to the CCS attributes the damages to an unidentified vehicle are particularly complex. In these cases the doubts about the actual participation of an unknown vehicle in the accident are very frequent and, if such vehicle exists, about whether the vehicle was the one responsible for the damages caused. Accident claims in which no witnesses appear are not infrequent, as is also the case where the witnesses who do appear do so at a later date alleging reasons that are not very convincing, or where the witnesses are connected with the victim by family ties or friendship.

Finally, in the accidents caused by vehicles insured by insolvent undertakings in the winding-up process, in most cases the CCS has to deal with old accidents, not attended to by the insolvent insurance undertaking and involved in litigation for some time.

To sum up, we can say that the claims to be addressed by the CCS in the preceding four covers, which it must handle in its capacity as the Guarantee Fund, are unusual claims clearly different from those normally dealt with by the insurance undertakings. These are claims which develop in an environment not at all favourable to immediacy in the determination of the liabilities concurring in the accident and the consequent quantification of the damages to be compensated. The claims filed late, those giving rise to doubts or suspicions, those filed with insufficient documentation or those “inherited” from an insolvent insurance undertaking are not precisely the kind to be settled quickly, nor do they rank among those most likely to be concluded through an out-of-court compromise.

The uniqueness of CCS’s experience in the subject concerning us here stems from the way in which it decided to reorient its compensation activity through the intensive and protective use of the Scale, in an effort to overcome all of the difficulties described earlier and take the claims out of the court system or prevent litigation, as the case may be, by furthering the attainment of friendly agreements in order to pay compensation to accident victims quickly.

This marked reorientation of its compensation activity, initiated in the five-year period from 1997 to 2001 and fully consolidated since that time, has been based on the intensive application of the Scale by the CCS, in line with the style expressly and very clearly promoted by the Ministerial Order of 5 March 1991, so frequently referred to here, that is, “according to the principles of sufficiency and speed”, and avoiding at all costs “its use in a negative manner, by having recourse to a restrictive application of the Scale”.

The CCS has found in the Scale a key instrument for protecting the interests of traffic accident victims and has applied it with protective criteria, in such a way that, whenever different and reasonable interpretations have existed on an issue raised in relation to the Scale, the CCS has chosen to apply favourable and not restrictive interpretative criteria for the injured party. This protective focus - fully justified by the status of the CCS as a public entity- has been accompanied by the simultaneous application of the necessary rigour by the CCS when undertaking an examination of requests for compensation which are insufficiently documented or not well-founded, if not outright abusive or presumably fraudulent.

In accordance with this protective focus, the CCS, for example, has generally paid compensation by applying the Scale in effect on the date of settlement of the claim, in line with the idea –included expressly and unequivocally by the new Scale- that the compensation damages incurred by the party responsible for the accident is a pecuniary debt.

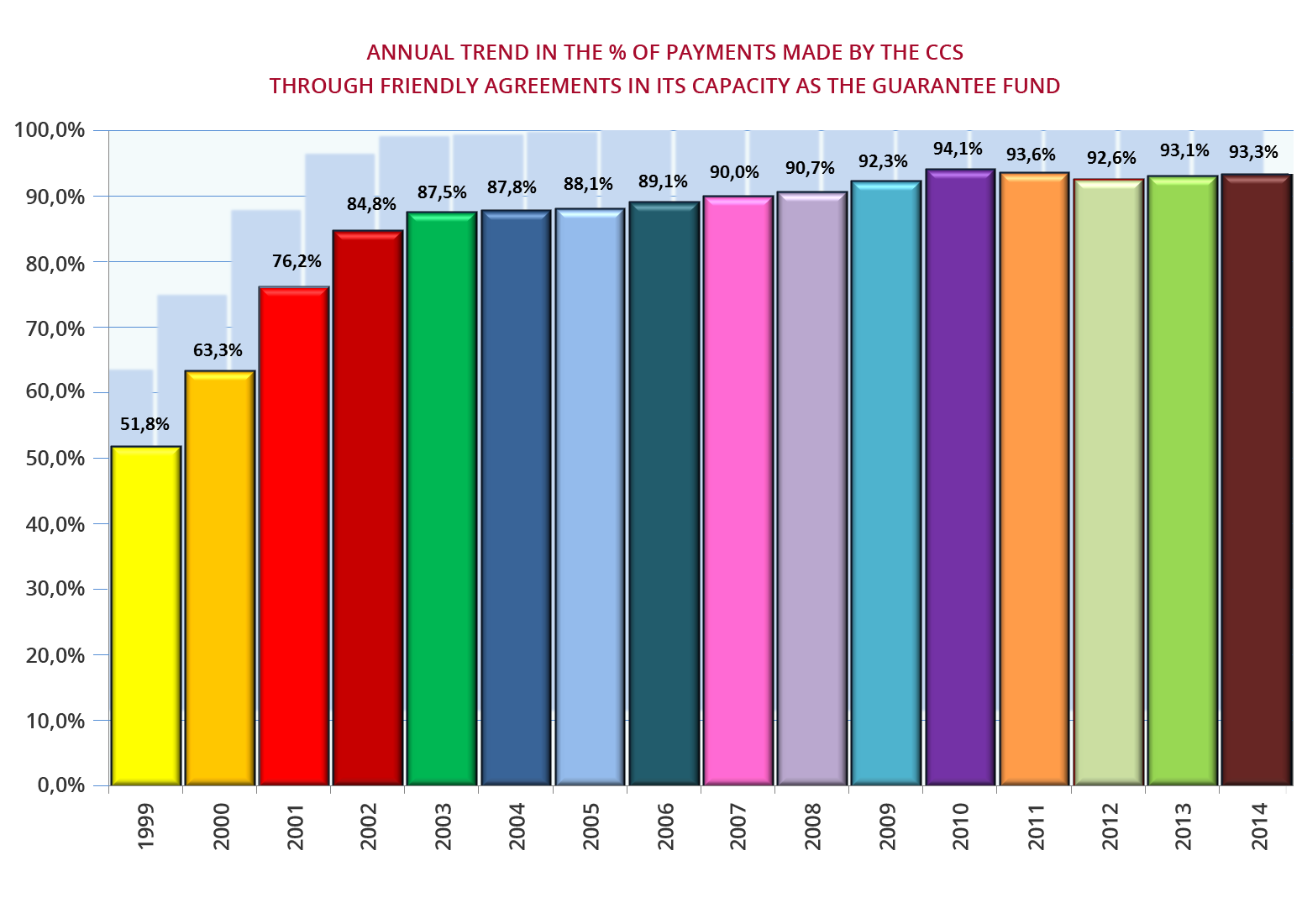

The effectiveness of the use of the Scale for avoiding undesired litigation and for reaching compromise agreements with the injured parties can be observed on the following chart, which shows the trend in the number of payments made through out-of-court agreements in a single year in relation to the total number of payments in that year.

If in 1999 there was still a significant percentage of judicial payments, in a matter of a very few years the compromise settlement culture was successfully inculcated among the CCS claims adjustors, and that culture, as can be seen in the very high percentage of the annual non-judicial payments, has been maintained since 2002 - 2003 in a very consolidated manner. The use of the Scale has significantly facilitated the smooth processing of these particularly difficult claims and the achievement of friendly agreements with the injured parties, a fact frequently recognised both by judges and magistrates as well as by associations of traffic accident victims.

The transcendental challenge now faced not only by the CCS but also by the Spanish insurance system overall is to maintain the spirit of friendly settlements and the speed in making compensation payments through a much more comprehensive and complex instrument, full of new developments, still lacking practical and consolidated criteria of application and inevitably generating, in its initial stage, frequent interpretative doubts.

Legislators have made their expected contribution towards facilitating a lengthy and progressively improved lifetime for this new Scale, by wisely taking up the initiative proposed by the CEX consisting of the creation of a Monitoring Committee, on which the accident victims and the insurance undertakings will be represented on an equal basis. This Committee, in turn, will contribute to detecting problems and imbalances and to making weighted proposals for improvements.

It is now up to the other players –insurance undertakings and CCS; victims and their representatives; judicial bodies; medical and legal experts– to contribute, with moderation and without losing sight of the general interest and the spirit of consensus, to peacefully overcoming the initial moments of inevitable doubts and possible needs for adjustments.